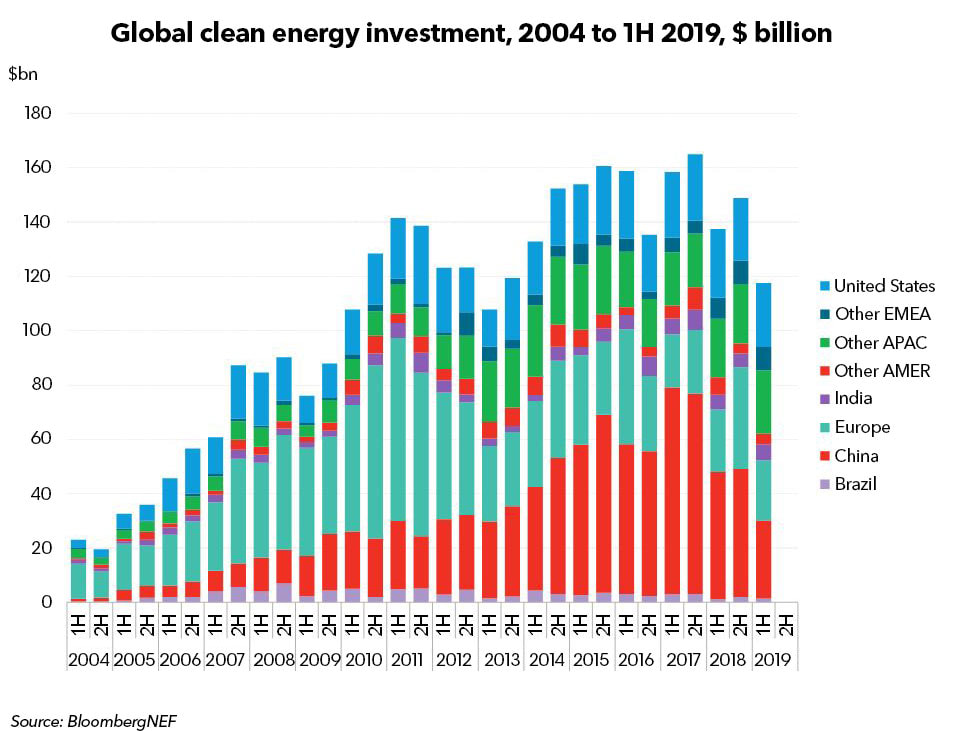

As we come to the end of the year 2019 (and the decade) the most sobering thing is the solid lack of progress in clean energy deployment and CO2 reduction. The thing that best exemplifies the lack of progress is the low, stagnant level of investment in clean energy. As I have discussed in many blog posts over the years, investment in clean energy has been relatively stable at about $250B/Y for most of the decade since 2011. As we close out 2019 and the decade, investment is actually down substantially. This is largely due to China restructuring their clean energy subsidy regime. This low world investment in clean energy regime shows no sign of improving and at this level is insufficient to even cap yearly CO2 emissions which continue to grow every year.

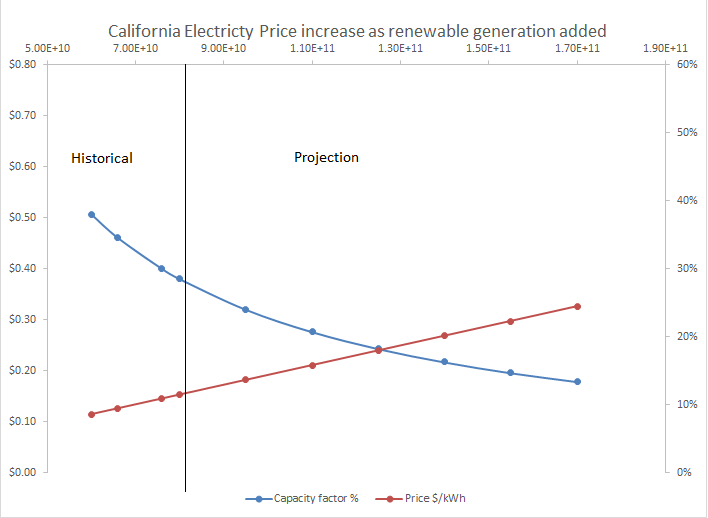

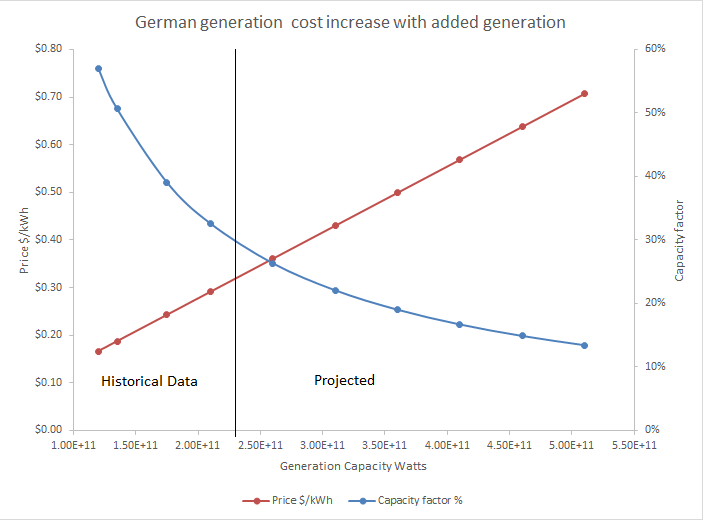

There has been substantial progress in reducing the cost of generation from wind and solar which has produced a false optimism among clean energy advocates that envisage a 100% clean energy world by 2050. When we are only adding a small amount of intermittent clean energy the additional costs are easy to ignore. However as I pointed out in recent blog posts, as the amount of intermittent clean energy added rises, the cost of electricity also rises for very predictable capacity factor reduction reasons. This is solid real world data from Germany and California.

So we have real world data on stagnant investment and real data on rising cost impediments to large scale intermittent clean energy deployment. The optimism of the potential for 100% renewables is sustained by theoretical academic models and simulations. In simulations there is a wide latitude for assumptions all of which may seem technically plausible but lack verification of practicality and defined paths to deployment at scale. One of the most elaborate of these models comes from Mark Jacobsen et al at Stanford. They recently released an update “Impacts of Green New Deal Energy Plans on Grid Stability, Costs, Jobs, Health, and Climate in 143 Countries”.

This report is full of data and inspires confidence in its vision. This is the curse of clean energy: the promise of light at the end of the tunnel and a brave new world opening up. Unfortunately the stagnant investment and real electricity price data do not match the vision.

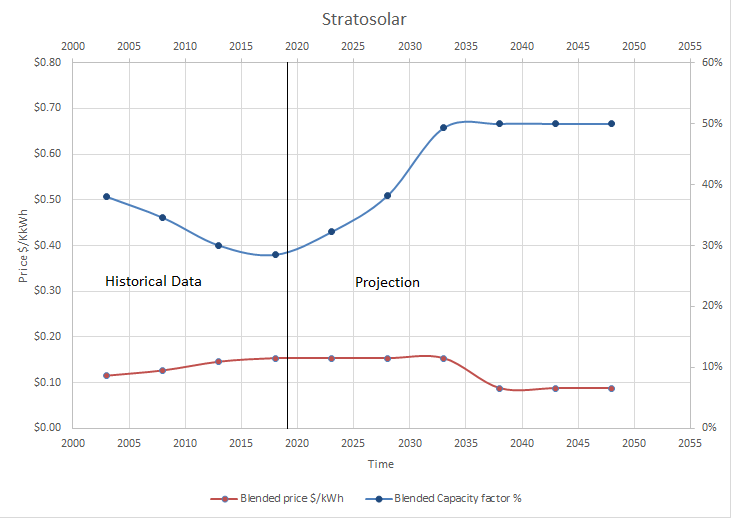

A Stratosolar solution does not require the myriad of complex adaptations to make intermittency practical that are used in these models. It has one big risk factor to demonstrate practicality. How long must we continue down a path that is demonstrably failing before we explore alternatives that can be proven cheaply and if proven can deliver limitless cheap clean energy.

By Edmund Kelly

There has been substantial progress in reducing the cost of generation from wind and solar which has produced a false optimism among clean energy advocates that envisage a 100% clean energy world by 2050. When we are only adding a small amount of intermittent clean energy the additional costs are easy to ignore. However as I pointed out in recent blog posts, as the amount of intermittent clean energy added rises, the cost of electricity also rises for very predictable capacity factor reduction reasons. This is solid real world data from Germany and California.

So we have real world data on stagnant investment and real data on rising cost impediments to large scale intermittent clean energy deployment. The optimism of the potential for 100% renewables is sustained by theoretical academic models and simulations. In simulations there is a wide latitude for assumptions all of which may seem technically plausible but lack verification of practicality and defined paths to deployment at scale. One of the most elaborate of these models comes from Mark Jacobsen et al at Stanford. They recently released an update “Impacts of Green New Deal Energy Plans on Grid Stability, Costs, Jobs, Health, and Climate in 143 Countries”.

This report is full of data and inspires confidence in its vision. This is the curse of clean energy: the promise of light at the end of the tunnel and a brave new world opening up. Unfortunately the stagnant investment and real electricity price data do not match the vision.

A Stratosolar solution does not require the myriad of complex adaptations to make intermittency practical that are used in these models. It has one big risk factor to demonstrate practicality. How long must we continue down a path that is demonstrably failing before we explore alternatives that can be proven cheaply and if proven can deliver limitless cheap clean energy.

By Edmund Kelly

RSS Feed

RSS Feed