|

This report titled “Beyond Boom and Bust” , was published in April 2012 and I commented on it in this blog post. It was the work of several bodies and individuals, including the Brookings Institute. It argued that US clean energy policy was producing boom and bust cycles, but making no progress in reducing atmospheric CO2. They advocated a more results driven “technology led” policy. The recent EPIA report on PV market outlook for 2014 to 2018 had an interesting section that described the recent behavior of the PV market in Europe as a series of unsynchronized national boom and busts that were hidden by looking at the overall European market statistics. To quote from page 31:

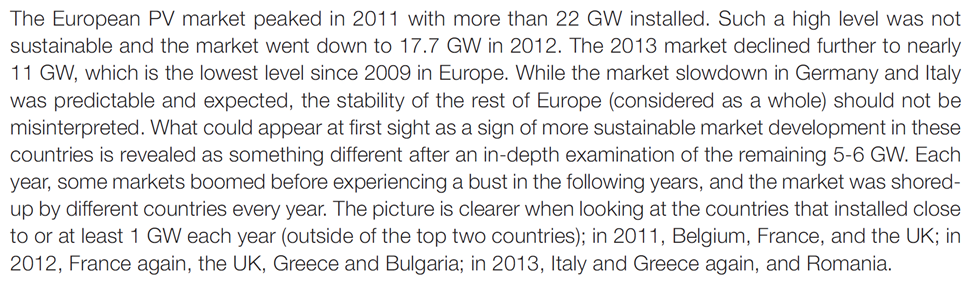

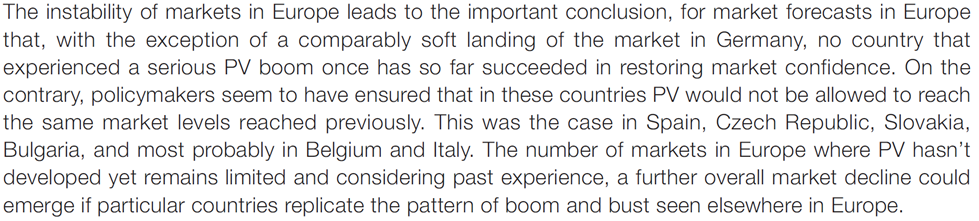

PV seems to have always and everywhere followed a path of governments introducing subsidies, investors responding enthusiastically producing a rapid growth boom. Governments then belatedly see the costs mount and reduce subsidies, causing a market bust. Then investor confidence is broken and difficult to restore. Europe has few countries that have not gone through this cycle. Europe has gone from being the biggest PV market to number three or four, with little sign of a likely recovery.

The recent US rapid PV growth is driven by US subsidies enabling profitable investment in PV. The expiration of the Investment Tax Credit in 2016 will burst this bubble, just like all the rest. The governments in Japan and China are early in the subsidy cycle so the boom phase is only building up. In a year or two the costs will be un-sustainable and the bust will inevitably follow. All of this makes it virtually impossible for PV to reduce in cost. Low and unpredictable PV market growth will not encourage investment in newer plant and equipment that can reduce costs. At current cost levels PV market cannot grow without more subsidies. As the boom and bust cycles clearly illustrate, more subsidy is unlikely to be forthcoming. As the “Beyond Boom and Bust” report argued, current US clean energy subsidy policies are not succeeding. They only considered the US, but as we can see, the problem is worldwide. Perhaps it is time to consider the “technology led” policy reforms they advocated. By Edmund Kelly

Comments

Now that 2012 is behind us it is useful to see how things have worked out in the PV market during 2012 and how they look going forward.

As my early 2011 blog posts predicted, there was little growth in 2012 over 2011. The overall GW installed in 2012 grew slightly over 2011 (from 27GW to about 29GW), largely because Germany installed 7.5GW, as opposed to their 3.5GW goal. The overall dollar size of the PV panel market shrank by about 50% as industry consolidation drove panel prices down to around $0.70/Wp and installed utility projects to about $2.40/Wp in the US. Projections going forward are for about a 20% annual increase in installed capacity. Panel prices will stabilize somewhere between $0.70 and $1.00 as the shakeout continues into 2013 and then slowly decline from there in future years as the installed capacity grows. This leaves prices still too high to compete without subsidies even in the best sunny locations. This means the market size is still determined by the amount of subsidy, which with reducing subsidies explains the modest growth projections (China and Japan are exceptions). PV has yet to become a significant % of the grid in any geography, so as yet additional costs for backup and transmission are not being counted. This will change going forward and act as a further brake on possible PV growth. Green advocates like Greenpeace need to become more realistic in their assessments. Current wind and solar will not make a significant impression on CO2 reduction before 2035 and currently could easily be adding to CO2 rather than reducing it. The impact is so small as not to be measurable in the current atmospheric CO2 levels. Unrealistic optimistic wishful thinking are damaging the prospects for any meaningful policy to reduce CO2. NREL and other researchers bring out studies that purport to show that the world could adapt to run on mostly wind and solar, but don’t spell out the costs. More importantly in a world where the US is a decreasing influence on energy and everyone has to act together, what the US does alone is increasingly irrelevant. As I keep repeating, a PV solution that enables today’s PV cells to produce cost competitive electricity without any subsidy, eliminates reliability and backup costs and long transmission lines, and does this for all geographies including cloudy and/or northern locations deserves some consideration. By Edmund Kelly My most recent posts have been about the bursting PV bubble. At first glance this may seem only distantly related to StratoSolar, but in fact it is central to the biggest obstacle we face. When presenting the technology, occasionally we get the observation that existing alternative energy technologies are on a path to imminent success, if they are not already at that point. When we don’t get the observation directly, it is always implied. This view is pretty universal among both the technical and business savvy individuals that comprise our usual audience and forms the basis for not seriously evaluating StratoSolar. If you see little benefit and high risk for a problem you believe solved, the intuitive reaction is to reject the outrageous new approach without too much thought.

Alternative energy advocates have hyped both wind and solar into a general perception that they are practical alternatives. The bursting solar bubble and the continuing scale of wind subsidies shows how far either is from economic viability. Actually the situation is much worse, because both are intermittent, and assessments that they can integrate into a grid have proven wildly optimistic. Wind, depending on its percentage of the grid may not even save CO2 or fuel, because of the loss of efficiency of the normal generation, and the losses of spinning backup. Solar is only likely to be viable in sunny locations with large populations if and when there is a storage solution. Objective projections by the IEA, EIA and others don’t foresee much of a market share for alternatives out to 2035. Alternative energy advocates are in a difficult position. They have no attractive alternatives and this distorts their objectivity, and leads to overselling. Unfortunately overselling eventually leads to a backlash that can be very damaging to long-term prospects. It’s unfortunate, but for StratoSolar to get serious attention, the perception of the imminent practicality of alternative energy solutions has to diminish, which is why we pay so much attention to the PV bubble bursting. Hopefully this will lead to more sober assessments of approaches like StratoSolar that attempt to solve the complete problem including cost, intermittency and geography and can realistically scale to solve the complete energy problem. To that end we have added a paper to the PV documents section on deploying StratoSolar in Japan, which illustrates the scale of a complete solution for a real economy and geography with particularly difficult constraints. There are also Japan deployment pictures in the PV Gallery. |

Archives

December 2023

Categories

All

|

RSS Feed

RSS Feed

|

© 2024 StratoSolar Inc. All rights reserved.

|

Contact Us

|