|

Its interesting that the two major alternatives to fossil fuel energy (wind+ solar and nuclear) are mostly at odds with each other. In the debate, they both point out the weaknesses of the other, and to an objective outsider clearly paint a picture where neither is a viable solution. The problems with cost overruns on new nuclear plants in the US and Europe have sharpened the debate recently with Toshiba’s announcement of massive losses from its Westinghouse division. The pointers at the bottom below show three perspectives on Toshiba’s woes.

My most recent blog posts have focused on the problems with intermittent wind and solar. Nuclear clearly has its problems too. Toshiba’s and others (Areva) problems at minimum show how hard current nuclear is, without even getting to how it could be modified to be more sustainable and load follow. With reactors being shut down in Europe, the US and Japan and cost overruns leading to no new orders, nuclear is not going anywhere. China is the only country adding any significant nuclear capacity. This would seem to end what had been seen as the beginnings of a nuclear revival. Most nuclear advocacy centers on new designs to remedy problems with current reactors. Nuclear takes a long time from experimental to demonstration to production power plants. Minimally the sequence takes decades and costs billions to tens of billions of dollars. So, nuclear power and wind and solar face similar problems. Neither are viable replacements for fossil fuels and it will take significant development of new unproven technologies to make them so. Compare this with StratoSolar. Much of StratoSolar is just today's PV. The unproven parts are relatively simple engineering based on existing mass produced technologies. To follow the nuclear model, the first step is to build an experimental platform. This could be done in less than a year for a few million dollars. An experimental nuclear reactor is many years and hundreds of millions of dollars. Relative to a new nuclear reactor, StratoSolar demonstration and production platform steps are equally as fast and low cost as the experimental platform. The point is that StratoSolar is no more speculative than wind, solar and nuclear, when the development paths of each that lead to viability are objectively analyzed. The perspective that wind, solar and nuclear are all unproven and speculative is not the perspective of their advocates. Wishful thinking rules the day. Recently Bill Gates led the founding of Breakthrough Energy Ventures (BEV), a fund to invest in long term energy ventures. Given Bill Gates fondness for nuclear power, funding nuclear power is probably the focus of the fund. Given the funding required to get to production plants, its very unlikely that a private fund could raise the tens of billions required even to develop one new plant. Presumably the plan is to fund the earlier cheaper development stages and persuade governments to foot the major bills. Perhaps we can persuade BEV to fund StratoSolar? It might be high risk but its cheap and fast. Its actually a typical venture funded opportunity. By Edmund Kelly Rod Adams: reporter http://www.theenergycollective.com/rodadams/2398838/toshiba-announces-6-3b-writedown-229m-construction-company-acquisition Jim Green: Friends of the earth: http://www.theenergycollective.com/energy-post/2399091/nuclear-safety-undermines-nuclear-economics Michael Schellenberger: The breakthrough institute http://www.theenergycollective.com/shellenberger/2398737/nuclear-industry-must-change-die

Comments

PV is not a free market. It is dominated by China and the peculiarities of the Chinese economy. China is both the largest manufacturer and the largest consumer of PV. This has all occurred extremely rapidly over about the last five years. 2017 appears to potentially be a year of reckoning for PV, as this blog article neatly summarizes. The total historical PV cumulative installed capacity is about 300GW, most of it installed over the last few years. 2016 Installed capacity alone was about 70GW, with about 30GW of that in China. US installed a record 12GW in 2016, driven by the potential expiration of subsidy incentives. Most projections have 2017 world PV installations falling well below the 2016 70GW due to reductions in China and the US, with no major new growth area to compensate.

These reductions stem in part from the limited ability of electricity grids to absorb PV. The long-term limit is based on the capacity factor limit of grids to absorb intermittent sources. We are far from this limit, but short term constraints are showing up at very low levels of PV penetration. China’s current limit is the lack of long distance transmission capacity to take the power from the deserts in the west to the users in the east. As discussed in this blog post, California is hitting problems due to the inability of fossil generation to ramp up and down quickly enough to compensate for rapidly changing PV generation as the sun sets. Advocates for PV are focused on the falling cost of PV generation and seem to assume that once PV becomes the lowest cost of generation the world will magically switch to solar energy. The reality is far from this rosy scenario. The real cost of PV electricity will increasingly have to factor in the additional costs needed to incorporate it into the electricity supply system. California is showing the need for storage at very low levels of penetration and China is showing the need for long distance HV-transmission. Both technologies are expensive and in need of development, particularly electricity storage. They are both additions to the current grid and both exceed the cost of PV generation. Add to this the geographical variability of solar, particularly at northern latitudes and the economic case for solar to be a large scale, economically viable supplier of electricity is far in the future. StratoSolar is low cost generation with low cost, fast response storage built in and no need for long distance transmission. It has no daytime intermittency problem and it works well at northern latitudes. It needs relatively minor short term development to prove its viability. In contrast, the storage and HVDC transmission technologies needed to make ground PV viable are in many ways more speculative, unproven and longer term than StratoSolar. By Edmund Kelly Large new supplies of Helium have recently been discovered by employing modern exploration tools. This discovery may be the tip of the iceberg. There is considerable potential for discovering a lot more. This could have positive implications for StratoSolar as it raises the possibility of using Helium rather than Hydrogen as the buoyancy gas for large scale platforms. There is a lot of concern about the safety of Hydrogen and the use of Helium is a simple fix. As discussed in a question in this FAQ, current world Helium supplies are too limited for large scale deployment of StratoSolar platforms and the cost is already prohibitive. Hydrogen is a viable buoyancy gas that can be safely used with proper attention to safety engineering. However, the image of the burning Hindenburg still banishes Hydrogen from consideration. Abundant Helium resolves this issue and significantly simplifies the engineering of StratoSolar platforms.

By Edmund Kelly The attached white paper is a more comprehensive look at the impact of higher energy costs on reducing GDP growth. This tells us two things. First, we are in serious economic trouble already with a low and declining rate of economic growth from the continually increasing cost of fossil fuels. Second, replacing fossil fuels with more expensive alternative energy sources will only make the problem worse. So far, wind and solar have been a relatively small economic factor, but growth to a level where they can contribute to a significant reduction in CO2 emissions would quickly get us into economic decline, and the political unrest that comes with economic decline. StratoSolar's lower cost of energy production than fossil fuels can reverse the current decline in the rate of economic growth by making energy cheaper on a continuing basis. By Edmund Kelly

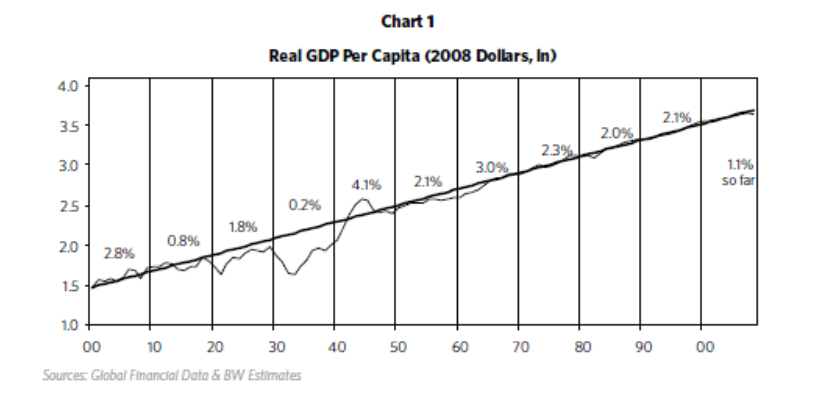

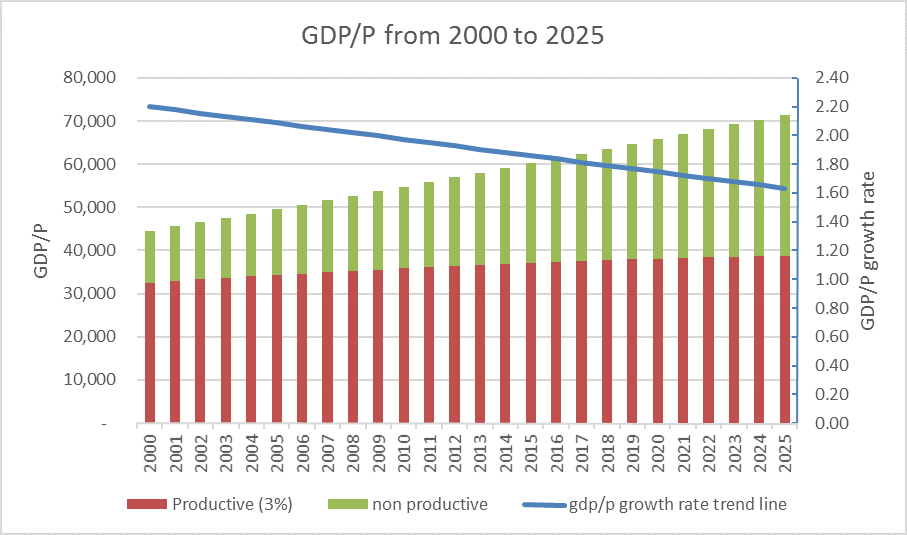

An argument against large scale deployment of alternative energy is the negative impact of the higher cost on gdp growth. The following is an attempt to quantify this effect based on the increasing cost of energy since around 1970. The modern world is based on sustained economic growth. As the chart below shows, US real gdp per capita has maintained an overall 2% per annum growth rate through depression, recessions and two world wars. This has been possible because of technological advances increasing the productivity of all economic sectors. Since around 1970, the cost of producing energy has steadily risen. Initially this was driven by the increasing cost of oil production, and more recently the cost of expensive alternative energy production has also become a significant factor. Energy is a significant part of gdp, so its share growing from around 5% to around 10% of gdp should clearly have been a drag on the growth rate of gdp, reducing it from its long term 2% per annum historical trend.  When we examine US GDP growth rate data for various periods from 1960 to today, regardless of the period chosen it is apparent that growth rates have been on a steadily declining trend. The straight line in the graph below shows a snapshot of the actual downward trend from 2000 to 2015 projected forward to 2025. The colored bars also illustrate a simple model that assumes the economy has two sectors. One sector has a high productivity growth rate of 3% and the other sector is stalled out with 0% productivity growth rate. To make the numbers fit the data we need to start with the non productive sector at 25% of GDP. This produces a breakdown like that shown, with the non productive sector continually increasing as the overall growth rate declines. These numbers imply that a larger sector of the economy than just energy is contributing to the recent decline in economic growth rate. Increased energy costs account for about a third of the decline by 2015. The other likely contributors to low growth rate are substantial parts of the financial sector, health care and education. This reduced rate of overall economic growth is causing severe economic problems already, with income inequality and stagnant wages. The problems will only get worse if the growth rate continues on its current downward trend. This illustrates that economic growth is a sensitive thing that cannot survive a large part of the economy becoming less productive. This should make it clear that a competitive, lower cost source of clean energy is a necessary condition for an energy transition that does not destroy economic growth. Current wind and solar are currently several times the needed lower cost and are reducing in cost at too low a rate to be an affordable solution for a long, long time. Other approaches like StratoSolar that can solve the problem without destroying the economy deserve some serious attention.

This white paper covers the topic of the reduction in economic growth caused by the increasing cost of energy.

By Edmund Kelly By Edmund Kelly

This article in next big future highlights the rapid advances in large scale desalination deployment that Israel has led over the last decade. Israel, a country of 8 million people, has gone from a precarious water supply situation to a position today where 50% of its water supply is from desalination and by 2020 it will be 70%. Fortuitously for Israel this has occurred while the Middle East is in the middle of a multi year drought which would otherwise have had a serious economic impact, as has occurred elsewhere in the Middle East. As this recent paper illustrates in detail, reverse osmosis (RO) desalination has been steadily improving and is being deployed on an increasingly large scale worldwide, not just in Israel. The Israeli company IDE is selling water from the latest plant at Sorek for 58 cents a cubic meter. That is about $690/acre-foot, or less than much of the water purchased in California, some of which costs as much as $1,200/acre-foot. As the paper illustrates there are strong prospects for further cost reduction. Reverse osmosis currently consumes about 3kWh of electricity to produce a cubic meter of water. At $0.06/kWh that is $0.18/m3 or about one third of the cost. Providing the energy for desalination from a cheap and sustainable, high utilization source would alleviate a major environmental concern that limits a broader acceptability of desalination, particularly in California. Currently wind and solar alternative energy sources are expensive and worse, have a low utilization. The low utilization means desalination plants would have an equally low utilization. The combination of high cost and low utilization makes desalination powered by current intermittent alternative energy multiple times the cost from fossil fuels. The StratoSolar solution of high utilization PV combined with gravity energy storage provides a cheap, high utilization, clean sustainable source of energy for desalination. Its lower cost over time will help further reduce the cost of clean water. The continuous cost reduction learning curve of RO desalination combined with StratoSolar electricity would reduce water costs to around $0.20/m3 ($230/acre-foot) by the early 2020s. This would make desalination the cheapest and most environmentally friendly source of water, potentially reducing some of the environmental impacts of the current exploitation of natural clean water sources. By Edmund Kelly A complete renewable energy solution requires the attributes of dispatch-ability and reliability of fossil fuel power plants at a lower cost of generation. PV panels have come down rapidly in price in recent years creating a wave of optimism for PV. A realistic analysis projects further price drops over time, but not at the recent precipitous rate of decline. Current PV price levels still need subsidy in all markets to generate electricity competitive with that from fossil fuels. Also PV is an unreliable and intermittent source of electricity that requires backup fossil fuel generation (or excess capacity and distribution) to handle unpredictable long duration weather outages and daily energy storage for nighttime generation. Currently there is no viable large scale energy storage solution other than pumped hydro. To provide renewable energy for less than fossil fuels, the combined cost of PV generation, backup generation and energy storage generation have to be less than the cost of generation from fossil fuels.

StratoSolar is a system solution that directly attacks all the problems of PV generation and transforms PV into a real, disruptive and transformative lower cost renewable energy solution.

StratoSolar is a combination of tried and true PV technology with a new unproven high altitude buoyant tethered platform technology. The risk is concentrated on the new technology of the buoyant tethered platform. Viability depends on whether buoyant tethered platforms can be built, deployed and not damaged or destroyed by environmental hazards over the 30 plus year lifetime of the power plant. Other risks are whether the predicted capital costs are achievable and possible regulatory impediments from the FAA and local authorities. The new buoyant tethered platforms are really novel structural engineering towers. Large scale structural engineering is a well established engineering discipline. Building the first of a new class of large scale structural engineering projects could be compared with other once novel large structural engineering projects, like steel framed skyscrapers, concrete dams, oil production platforms or steel suspension bridges. This class of project always initially stretch human credibility but actually rarely fail because the structural engineering discipline is very robust. The same reasoning applies to StratoSolar platforms. This report titled “Beyond Boom and Bust” , was published in April 2012 and I commented on it in this blog post. It was the work of several bodies and individuals, including the Brookings Institute. It argued that US clean energy policy was producing boom and bust cycles, but making no progress in reducing atmospheric CO2. They advocated a more results driven “technology led” policy. The recent EPIA report on PV market outlook for 2014 to 2018 had an interesting section that described the recent behavior of the PV market in Europe as a series of unsynchronized national boom and busts that were hidden by looking at the overall European market statistics. To quote from page 31:

PV seems to have always and everywhere followed a path of governments introducing subsidies, investors responding enthusiastically producing a rapid growth boom. Governments then belatedly see the costs mount and reduce subsidies, causing a market bust. Then investor confidence is broken and difficult to restore. Europe has few countries that have not gone through this cycle. Europe has gone from being the biggest PV market to number three or four, with little sign of a likely recovery.

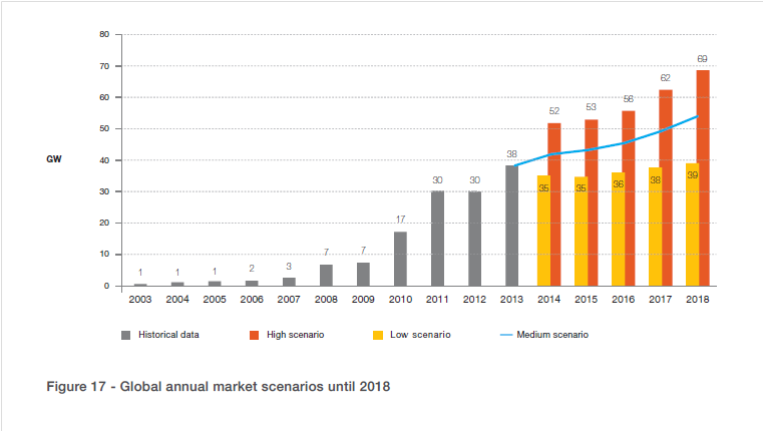

The recent US rapid PV growth is driven by US subsidies enabling profitable investment in PV. The expiration of the Investment Tax Credit in 2016 will burst this bubble, just like all the rest. The governments in Japan and China are early in the subsidy cycle so the boom phase is only building up. In a year or two the costs will be un-sustainable and the bust will inevitably follow. All of this makes it virtually impossible for PV to reduce in cost. Low and unpredictable PV market growth will not encourage investment in newer plant and equipment that can reduce costs. At current cost levels PV market cannot grow without more subsidies. As the boom and bust cycles clearly illustrate, more subsidy is unlikely to be forthcoming. As the “Beyond Boom and Bust” report argued, current US clean energy subsidy policies are not succeeding. They only considered the US, but as we can see, the problem is worldwide. Perhaps it is time to consider the “technology led” policy reforms they advocated. By Edmund Kelly This sixty page report EPIA Global Market Outlook for Photovoltaics 2014-2018 paints a pretty accurate picture of the recent history of the global PV market and has realistic projections for the near term. It has detailed information for each geography and market segment. The graph below from the report shows the near term overall world market projection with optimistic, pessimistic and realistic scenarios. The realistic middle scenario shows slow overall market growth, but no spectacular take off. The conclusion of the report is a welcome return to reality about the future prospects for PV and a marked contrast to the over optimistic assessments that still seem to pervade the PV business. The central point of the conclusion is that “ The PV market remains in most countries a policy driven market, as shown by the significant market decreases in countries where harmful and retrospective political measures have been taken.” A policy driven market is a euphemism for a subsidy driven market. This lines up with my assessments of the prospects for PV business over the last several years as published in this blog. PV growing at this rate is fine for the PV business, but will not make PV a significant source of electricity anytime soon. It is not sufficient growth to drive costs down, so the business will need subsidy for the foreseeable future. The conclusion of the report backs this assessment as it clearly states that growth is dependent on “sustainable support schemes”. i.e. more subsidies. At some point those that promote current policies in the belief that they will reduce CO2 emissions have to stand back and make a realistic assessment of what they are accomplishing, or more accurately failing to accomplish. By putting all their eggs in the current wind and solar baskets, they are actually precluding investment in possibly better technologies. The psychology seems to be driven by a fear that admitting that current wind and solar are failing, will lead to nothing being done, and something is better than nothing. The reality is that investing only in failure guarantees failure. By Edmund Kelly

In the computer industry there is the concept of “computer platforms” Examples are the PC platform, the MAC platform and the Android platform. The platforms are combinations of hardware and software that act as a standard basis for many applications. In a different more physical way, StratoSolar technology has evolved into a platform for multiple applications.

We initially developed the technology targeted at solar PV electricity generation. Doing this involved solving a series of significant problems that led us to methods for the design, construction and deployment of small to large scale modular, buoyant-platform systems. The first additional platform application beyond PV generation we serendipitously discovered was gravity energy storage. This is very synergistic with intermittent PV generation. Cost effective energy storage is an area in great demand without any clear solution today . As well as complementing PV generation for the energy market, this also means that small stand alone platforms can supply energy for other platform applications. Such an emerging application is wide area wireless internet communications. The platforms we have evolved can quickly and cheaply provide very cost effective wireless internet communications. Other more conventional broadcast and cellular communications can also easily benefit. One thing leads to another. The use of winches to store energy by transporting weights from the ground to the platform and 20km altitude also enables the transport of goods, equipment, and ultimately, people from the ground to platforms at 20km and back. This means that communications and observation equipment can be deployed and recovered without bringing platforms down to the ground. The weights involved with gravity energy storage can get to several hundred tonnes. This leads to another possible application; containerized goods transportation. At various times attempts have been made to revive the use of airships without success. Airships suffer from their fragility. Within the troposphere violent and unexpected weather can destroy airships, either in flight, or more commonly in accidents when near the ground for docking and undocking. However, large stratospheric airships based on the StratoSolar construction method could carry payloads of several hundred tonnes between platforms while remaining permanently in the stratosphere. They would be powered by fuel delivered to the platforms, perhaps augmented with solar energy during the day. Containers would be transported with winches up to a platform, transferred to a docked airship, transported by airship to another platform where the airship docks and the containers are transferred to the platform and lowered with winches to the ground. Airships would be relatively cheap to buy at around $5M, cheap to operate, and would transport goods at about 100km/h from platforms that can be positioned anywhere. The cost of transportation would be somewhere between ships and aircraft, perhaps similar to trucks, but would be point to point and relatively high speed. Transportation is currently a long shot for StratoSolar, but indicates how a technology can evolve far from its original source. Many other expected and unexpected StratoSolar platform applications will inevitably evolve. |

Archives

December 2023

Categories

All

|

||||

RSS Feed

RSS Feed

|

© 2024 StratoSolar Inc. All rights reserved.

|

Contact Us

|