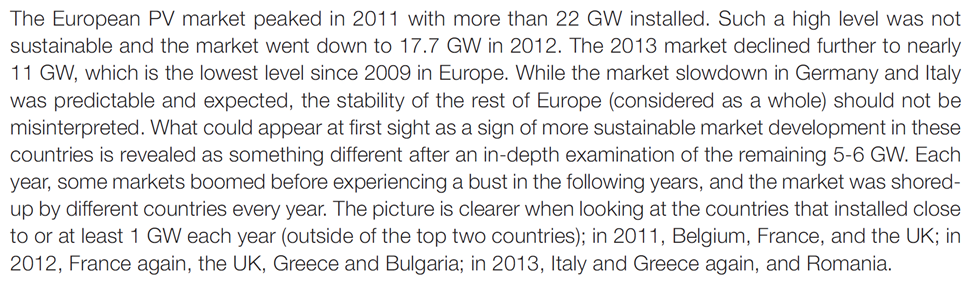

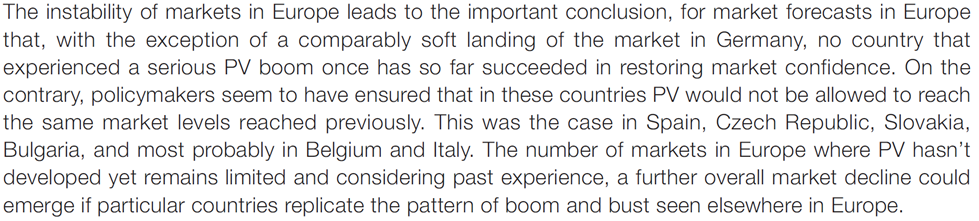

|

This report titled “Beyond Boom and Bust” , was published in April 2012 and I commented on it in this blog post. It was the work of several bodies and individuals, including the Brookings Institute. It argued that US clean energy policy was producing boom and bust cycles, but making no progress in reducing atmospheric CO2. They advocated a more results driven “technology led” policy. The recent EPIA report on PV market outlook for 2014 to 2018 had an interesting section that described the recent behavior of the PV market in Europe as a series of unsynchronized national boom and busts that were hidden by looking at the overall European market statistics. To quote from page 31:

PV seems to have always and everywhere followed a path of governments introducing subsidies, investors responding enthusiastically producing a rapid growth boom. Governments then belatedly see the costs mount and reduce subsidies, causing a market bust. Then investor confidence is broken and difficult to restore. Europe has few countries that have not gone through this cycle. Europe has gone from being the biggest PV market to number three or four, with little sign of a likely recovery.

The recent US rapid PV growth is driven by US subsidies enabling profitable investment in PV. The expiration of the Investment Tax Credit in 2016 will burst this bubble, just like all the rest. The governments in Japan and China are early in the subsidy cycle so the boom phase is only building up. In a year or two the costs will be un-sustainable and the bust will inevitably follow. All of this makes it virtually impossible for PV to reduce in cost. Low and unpredictable PV market growth will not encourage investment in newer plant and equipment that can reduce costs. At current cost levels PV market cannot grow without more subsidies. As the boom and bust cycles clearly illustrate, more subsidy is unlikely to be forthcoming. As the “Beyond Boom and Bust” report argued, current US clean energy subsidy policies are not succeeding. They only considered the US, but as we can see, the problem is worldwide. Perhaps it is time to consider the “technology led” policy reforms they advocated. By Edmund Kelly

Comments

Just a brief post that backs up previous posts on PV prices ticking up as the market stabilizes. This link is about GTM's near term PV price predictions. GTM publishes market research on the PV business. They are usually bullish and over optimistic.

This is good news for the PV business, as it means that it is finally getting to a more healthy footing after several years of disarray. This is mostly because China decided to support it's PV investments by subsidizing local demand within China. It will be interesting to see how far this goes, and also it will be interesting to see how long the recent surge in Japan lasts, now that they are adopting far more limited and realistically achievable CO2 emissions reduction goals. The deeper reality is that PV panels at these prices produce electricity that is still too expensive without subsidy in almost all markets. What is called grid parity for rooftop solar is now achievable in a few markets, but this is only because retail electricity is an overpriced monopoly in those markets. Solar with current subsidy levels is a stable business, but its not likely to grow to a size that will have an impact on CO2 emissions reduction. Hopefully the failure of over optimistic projections of PV price reductions based on short term extrapolations will sober up the eternal optimists and get some sense back into discussions of viable and realistic ways to reduce CO2 emissions. I doubt it. Published By Edmund Kelly Thisarticle in Renewables Energy Focus magazine provides more details on the state of the PV market as companies report their earnings. SPV Market Research puts the PV panel market in 2012 at 25GWp and $20B. Panel maker losses exceed $4B. This comes as Suntech the number six PV panel manufacturer declares bankruptcy.

2013 is not shaping up as much better than 2012. Major shifts in regional demand are underway, driven by where the subsidies are growing or declining. European demand is shrinking with reduced subsidy, but China has a profitable FIT and a goal of 10GW, and the generous FIT in Japan is projected to see 6GW installed. The Japanese growth will be met by Japanese panel makers despite their lack of market competitiveness, which may not help the PV business generally. Current panel prices combined with subsidies are also driving growth in the US(primarily California), which may see 5GW installed in 2013. The story is the same everywhere. Subsidies drive the market, and their amount determines the market size. The overall PV market is not likely to grow significantly in 2013 over 2012. As prices stabilize, and even rise a bit to restore profitability, the historical learning curve of PV panel price versus cumulative volume is still holding up very well. This is important to understand as it establishes the realistic fundamentals that should drive expectations for what can be achieved by PV. There has been a tendency to take an optimistic view of PV competitiveness based on extrapolating short term trends, or localized successes (like Germany) driven by large subsidies. PV has made great strides, but is still only competitive with a large subsidy in normal geography, or with a smaller subsidy in a sunny geography like California. The historical learning curve will take many years of current production rates to get PV panel prices down to competitive levels. To put things in perspective, PV on a world average has less than a 15% utilization. StratoSolar is 40% utilization on average. For ground PV panels to match StratoSolar, prices will have to more than halve from current levels to about $0.30/Watt. This will take a long time, perhaps decades. It’s a catch 22 for ground PV. Prices will only fall with volume, but volume will only happen with lower prices. StratoSolar competitive energy pricing has the potential to fundamentally change the energy market by driving PV volume installation now. By Edmund Kelly Now that 2012 is behind us it is useful to see how things have worked out in the PV market during 2012 and how they look going forward.

As my early 2011 blog posts predicted, there was little growth in 2012 over 2011. The overall GW installed in 2012 grew slightly over 2011 (from 27GW to about 29GW), largely because Germany installed 7.5GW, as opposed to their 3.5GW goal. The overall dollar size of the PV panel market shrank by about 50% as industry consolidation drove panel prices down to around $0.70/Wp and installed utility projects to about $2.40/Wp in the US. Projections going forward are for about a 20% annual increase in installed capacity. Panel prices will stabilize somewhere between $0.70 and $1.00 as the shakeout continues into 2013 and then slowly decline from there in future years as the installed capacity grows. This leaves prices still too high to compete without subsidies even in the best sunny locations. This means the market size is still determined by the amount of subsidy, which with reducing subsidies explains the modest growth projections (China and Japan are exceptions). PV has yet to become a significant % of the grid in any geography, so as yet additional costs for backup and transmission are not being counted. This will change going forward and act as a further brake on possible PV growth. Green advocates like Greenpeace need to become more realistic in their assessments. Current wind and solar will not make a significant impression on CO2 reduction before 2035 and currently could easily be adding to CO2 rather than reducing it. The impact is so small as not to be measurable in the current atmospheric CO2 levels. Unrealistic optimistic wishful thinking are damaging the prospects for any meaningful policy to reduce CO2. NREL and other researchers bring out studies that purport to show that the world could adapt to run on mostly wind and solar, but don’t spell out the costs. More importantly in a world where the US is a decreasing influence on energy and everyone has to act together, what the US does alone is increasingly irrelevant. As I keep repeating, a PV solution that enables today’s PV cells to produce cost competitive electricity without any subsidy, eliminates reliability and backup costs and long transmission lines, and does this for all geographies including cloudy and/or northern locations deserves some consideration. By Edmund Kelly The last post was about boom and bust in US shale gas, and previous posts have been about boom and bust in the PV industry. Both busts are similar in dollar terms and are occurring simultaneously, with many billions of investment mis-allocated. Both are also similar in the confusion and mis-information they engender.

Previous posts have covered the overcapacity and restructuring of the PV business in general terms. The long and growing list of specific bankruptcies and larger firms withdrawing from the market reinforces the grim reality of the situation. However, there continues to be regular articles and posts that ignore the underlying market realities and interpret continually falling panel prices as a sign of industry viability rather than industry decline. Some even go so far as to project the last few years of dramatic price decline forward and anticipate lower prices and a golden age for solar deployment. A telling statistic for projecting future PV manufacturing capacity growth is the purchasing of capital equipment needed to build PV plants. These articles cover the 80% decline in the solar equipment supply business and the bankruptcies and layoffs. As existing capacity is being destroyed through retrenchment and bankruptcy and no new capacity is being built, eventually supply will balance demand and the surviving manufacturers currently selling at or below cost will raise prices to become economically viable. The historic long term learning curve of 20% reduction in PV panel prices with each doubling of cumulative capacity still seems to be the best price predictor, as it has been for over thirty years. This would predict current PV panel prices of around $1.00/Wp which seems a likely point for prices to stabilize maybe next year (2013). Given the cyclic boom and bust nature of the business prices may not decline from $1/Wp for several years. This does not foretell a golden age of PV growth as prices at this level still need substantial subsidies to be market competitive. The amount of subsidy determines market size. Subsidy is in general decline. There is no driver for market growth other than fickle and limited government support. By Edmund Kelly US clean energy subsidies declining from $44B in 2009 to $16B in 2012 and probably $11B by 2014.5/14/2012 This New York Times article outlines the decline and credits the Brookings Institution, The World resources foundation, and The Breakthrough Institute. They jointly authored the following report “Beyond Boom and Bust” that details the decline and policy changes that they argue would make for a more sustainable subsidy regime. Unfortunately the current political situation does not bode well for reform, particularly if it costs money.

The current subsidy regime is boom and bust and not focused on technology improvement. It is classic government subsidies that encourage the status quo and create a class of companies that live on the subsidies without incentive to improve and who lobby to maintain the subsidies regardless of the benefit or lack thereof. It also funnels money to favored constituencies like government contractors and peer reviewed scientists. The main focus should be on technologies that have a realistic chance of economic viability with an honest accounting of costs associated with intermittency and geographic isolation. Too much of alternative energy is over optimism and pass the buck accounting. When we launched the PV version of the StratoSolar web site early last year, one of our central themes was the unsustainable cost of PV subsidy. Events in the second half of 2011 seem to bear out this prediction with a vengeance. Overly generous European FIT subsidies created a PV supply bubble that has now burst. In the last few years Germany alone has invested over $100B in PV and German electricity consumers will spend over $200B in excess electricity costs paying off this investment over the next 20 years. There is a growing political backlash as the extent of the costs become apparent. Germany is aiming to limit new installed PV capacity to an average of 3GWp in 2012 and subsequent years, down from around 7.5GWp in 2010 and 2011. Italy, in the grip of austerity is aiming for 1.4GWp in 2012, down from 6.9GWp in 2011. Italy and Germany combined were about 60% of the entire world PV market in 2010 (11GWp of 16GWp) and 2011 (14.4GWp of 23GWp). Lower panel prices and continuing subsidies should lead to some growth outside of Europe, particularly in the US and China, but not enough to make up the European shortfall. Optimistically 2012 world PV installations might be 23GWp, but a more realistic estimate would be around 16GWp The bottom line is that growth in the PV industry is going to be much lower going forward. PV panels are being sold below cost as a major industry restructuring is eliminating the oversupply from thousands of uncompetitive big and small PV businesses worldwide, including China. PV panel prices will stabilize at around $1.00/Wp but at this price level the slower growth will lead to decades of PV panel prices too high to make PV electricity competitive without subsidies even in the best markets like California with lots of sunshine and high electricity prices. This is borne out in the current small solar energy market size projections from the EIA, the IEA, the World Bank and others. Germany is an object lesson in all the problems of current PV technology. Being a cloudy northern country, its panels make less than half the electricity they would in southern California or Spain. Its installed 25GWp of PV only has a utilization of about 8% and produces the power of about 3GW of gas, coal or nuclear plants. However the installed PV capacity is sufficiently large (providing only 3% of total electricity) that the unpredictable intermittent nature of the supply is already causing problems for the German electricity grid. The uncertain PV capacity cannot count against maximum electricity demand and is effectively an expensive fuel saver that cannot replace existing capacity such as nuclear. 25GWp of StratoSolar PV in Germany would produce the power of over 10GW of gas, coal or nuclear power plants, and the fully predictable electricity would integrate easily into the grid, add to supply capacity and support the goal of replacing nuclear power. At today’s PV prices the unsubsidized electricity produced would be considerably cheaper than current German electricity prices. This is a stark contrast in the possible outcomes for the future of PV. Solar energy is the most abundant clean energy resource, widely accepted as capable of providing for all world energy needs. PV technology has made enormous strides and has clearly demonstrated its practicality and scalability. However it is still at least a factor of two too expensive at the best sunny locations and on its well-proven learning curve it will take a cumulative installed capacity of between 200GWp and 500GWp for the cost to halve. The 2011 cumulative installed PV capacity was about 62GWp and at likely PV installation rates getting to 300GWp will take at least a decade. This will not solve the problems of unreliable supply due to weather or the lower utilizations at cloudy northern locations. Stratospheric PV platforms solve all three problems (cost, reliability, utilization) and would seem to be a reasonable technology to make PV electricity practical today as opposed to the distinct possibility of never as government subsidies continue to disappear. |

Archives

December 2023

Categories

All

|

RSS Feed

RSS Feed

|

© 2024 StratoSolar Inc. All rights reserved.

|

Contact Us

|