|

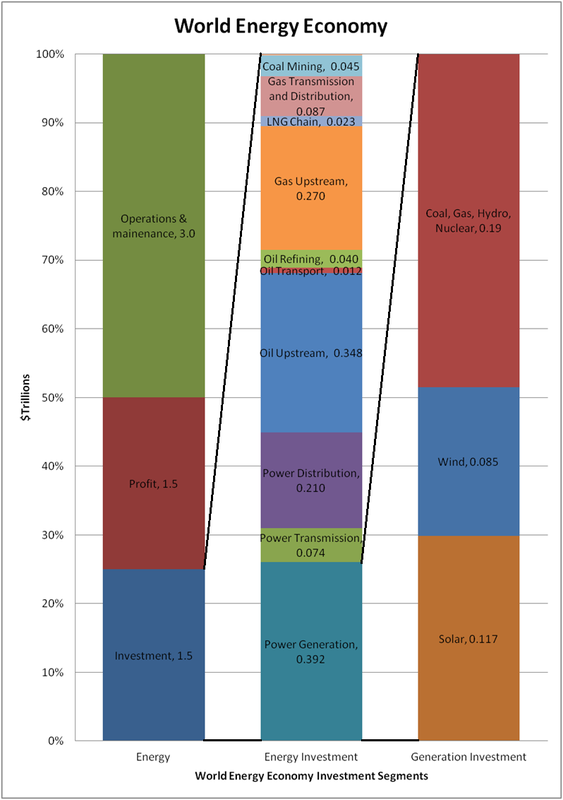

This chart visually illustrates the economics of energy discussed in the previous post. The left column shows all major energy segments. The middle column expands the energy investment segment and the right column expands the power generation investment segment. The numbers in each segment are Trillions of dollars. Its interesting that Solar is the biggest segment of power generation investment but it provides the lowest average power, a testament to the political power of renewable energy. By Edmund Kelly

Comments

Looking at the money, for 2013, world GDP was $72T, of which energy was $6T, or about 8% of GDP. That $6T can be thought of as the income of the overall energy industry. This income balances with industry profit, investment and O&M. From IEA data the energy industry investment part was about $1.5T, of which about $0.8T was in oil and natural gas infrastructure, $0.4T was investment in electricity generation and $0.3T was investment on electricity transmission and distribution.

From Bloomberg data, investment in wind and solar generation in 2013 was about $200B, with additional clean tech investment of about $50B on smart grid, biomass and bio fuels. Some of the investment in transmission and distribution is to integrate wind and solar and some smart grid spending is also related to wind and solar integration. So current investment in clean energy generation is over half of all investment in electricity generation . I have to admit I found this surprising. I always see alternative energy as the underdog, not the biggest player. That $200B bought about 45GW ($82B) of nameplate wind and about 35GW ($114B) of nameplate solar. Using average generation as the metric, conventional power plant capacity runs on average at about 50% utilization worldwide, so the world’s almost 6TW installed capacity generates an average 3TW of power. The 45GW of new wind generates an average of about 12GW and the 35GW of new solar generates an average of about 5GW, for a total of about 17GW of new average generation. That's 17/3000 or about 0.5% of current average electricity generation. The other $200B bought about 140GW of coal, gas, hydro and Nuclear power plants, mostly in China and India, that generate more than 70GW of average power or about four times the 17GW average of the new wind and solar. When we account for the cost of fuel, wind and solar electricity averages about two to three times the cost of electricity from other sources. Most of the investment in new electricity generation is driven by economic growth which needs to add about 3% of new generation every year. If just that increase was met with current wind and solar, it would cost close to $1T/y. That does not cover replacing the existing generation. Of the $200B spent for wind and solar, government subsidies account for at least half, or $100B. This is a look at the money. The bottom line is that wind and solar are already the biggest money part of electricity generation but are not providing much electricity. To scale wind and solar up just to meet current new generation demand would mean they would probably be the biggest industry on the planet. By Edmund Kelly Alternative energy exists solely because of a political will to make it so. It has been uneconomic from its modern inception in the 1970's, driven by the first oil crises. As a result, market driven economic viability has never been a central part of the alternative energy mindset. At its core it has been driven by two perceptions. The first was simply the need for a clean fossil fuel replacement largely regardless of cost. The second was that given time, costs would reduce to make them more acceptable.

The political will influenced government to provide subsidies to nurture the business. These subsidies now exceed $100B/y of investment worldwide and prop up a total investment of about $250B/y. However a business that depends so heavily on government support is subject to all the problems of such reliance. Firstly government support is volatile, driven by who wins elections. Secondly, subsidized industries are notoriously inefficient. Any long term subsidy regime encourages business that live off the subsidies with little or no incentive to improve. The perception that costs would reduce has been borne out by time, but the path has been a rocky one. The recent history of PV shows the erratic nature of this progress. On a day to day basis no one sees the big picture. When PV prices were stable for a decade, the perception was of stagnation which led to betting on thin film PV. When prices were falling the perception was they would continue to fall, regardless of fundamentals. Also, market size of a heavily subsidized industry is not perceived as inextricably tied to the size of subsidy. If government continues to support the PV business, costs will decline to a point where PV is competitive for some fraction of energy for sunny locations, but to be a complete solution other technologies like long distance transmission and storage have to become economically viable as well. The current rate of improvement put that point out beyond 2050. This is the status quo. Governments willing to provide limited subsidy, a business happy to live of this subsidy with its current size and rate of growth and an alternative energy political consensus that thinks this is actually working. This status quo is not reducing CO2 emissions and will not reduce CO2 emissions out to 2050. Realists point out that change of the degree necessary to reduce CO2 takes many decades and huge political will. While alternative energy imposes large new costs, the current small political will for change is directly measured by the small amount we are collectively willing to pay for subsidies. The only way to increase the political will is to reduce the cost at a faster rate or better yet turn things around and make clean energy an economic benefit. This perception is sadly lacking. The optimists place their hope in technological breakthroughs, and so we get daily updates on basic research, most of which we know will go nowhere, but create the illusion of progress. The sad reality is that basic research takes decades to make it from the lab to the market and decades more to achieve large scale. To scale quickly a technology needs both a long gestation to viability and to be mass producible. PV has recently demonstrated that it is at this point. The rapid scalability has surprised governments that provided subsidies assuming a slower ability to scale. Germany spent over $150B in two years for about 15GW before they adjusted. China just ramped to over 12GW in one year from a standing start for a lot less. So PV technology is at a point where we can make and deploy as much as we can afford. The problem is the high cost of the resulting electricity, especially if you count the costs of intermittency and storage, is just too much money for economies to sustain. StratoSolar is only PV in a new location. It reduces the cost of resulting PV electricity to market competitive levels and increases the reliability of the supply. There is no new technology or resource that limits its ability to scale. If it is proven viable, the major thing that needs to scale is PV manufacturing, the thing that has already demonstrated scalability. This is a lot like computers in the late 1980s. A large CMOS semiconductor manufacturing business had matured and companies like Sun Microsystems that built computers based on this technology rapidly scaled to volume in the millions. This pattern repeated itself for PCs in the 10s to 100s of millions and recently for mobile phones in the billions, as the cost of computers reduced with volume over time. The common elements are ability to scale supply and an affordable product with sufficient demand to match the supply. From an investment perspective the risk is like betting on a Sun Microsystems. They had engineering and market risk, but they were fundamentally enabled by available semiconductor technology. They were small investments in small teams that integrated existing technologies to build new products for very large new businesses. The market demand they produced could be met by the scalable semiconductor supply. Similarly, StratoSolar can create a demand that can be met by a scalable PV semiconductor supply. It’s continuing the triumph of the semiconductor age. by Edmund Kelly

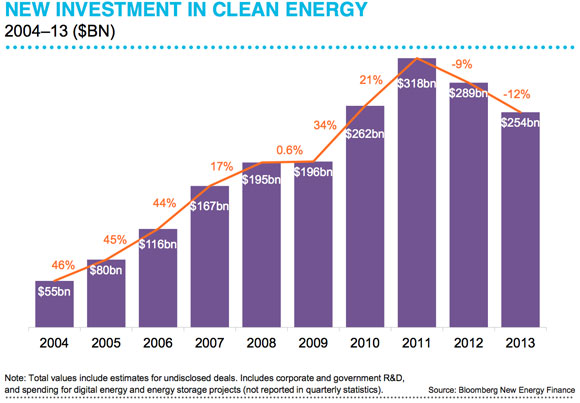

This Bloomberg graph shows world investment in clean energy declining over recent years. These declines are due to reducing government subsidies in turn reducing investment. This illustrates that government subsidies drive the market, a point that is rarely discussed, but is extremely important if you want to predict future market trends, as Bloomberg tries to do. If you read the analysis and projections, the fact that they depend almost 100% on predicting subsidies is never really stated. That’s because government actions are fickle and hard to impossible predict for timescales of years.

A bigger issue is that market size is determined by the amount of subsidy. At least one half of the clean energy investment shown is from subsidies. That is a minimum of $125B in 2013. Given that to make a significant impact on energy, we need to provide ten to one hundred times current yearly wind and solar alternative energy capacity additions, the implication is very large government subsidies of $1.25T/y to $12.5T/y. However, overall world subsidies seem set to decline further in 2014 and beyond, not grow. Europe has scaled back its clean energy agenda and the US with cheap gas is likely to reduce subsidies even more. Growth in China and India is slowing. Wind and solar power generation costs may reduce, but transmission, storage and other infrastructure costs will easily make up for this. None of this bodes well for reducing CO2 for the foreseeable future. The only rational strategy is to get an energy source that does not need subsidies to be a profitable investment. Wind and Solar cannot do this. As the numbers show, wind and solar are very large business and can survive and profit within the reduced subsidy domain. They can live happily and profitably off of current subsidies while blocking any potential competitors from any serious attention. While clean energy advocates continue to believe that wind and solar are the only answer, and consider any position that questions this as heresy, no progress can be made. By Edmund Kelly This is the Solve For <X> hosted hangout on air for StratoSolar video recording with the addition of pictures when referenced in the discussion. The length of the video and the dialogue is unaltered.

On Tuesday Jan 14th, between 10:00 and 10:30am PST, Solve for X is hosting a google+ hangout on air for StratoSolar. It's a hosted event where I'm asked a series of questions by a moderator and the audience can also ask questions. I have never done anything like this so I'm not really sure how it will work, but people can watch and participate live and there ends up being a YouTube recording of the event.

The link https://plus.google.com/u/0/events/cv1m6fasvccse8uvlnlk9n0gf4g is to sign up to attend the hangout, post questions ahead of time, and watch it when it happens on the 14th Another way to ask questions during the event would be to tweet me at @edkellyus It's an interesting experiment. Please sign up if you can and let others that might be interested know as well. Also, as I mentioned previously, the StratoSolar solve for x moonshot video has got high ratings on the solve for x site. If you login you can rate the video in various ways. If you have not done this already, please do. https://www.solveforx.com/moonshots/stratosolar-edmund-kelly Edmund Kelly The holy grail of alternative energy is practical, affordable energy storage. Without this, wind and solar energy can only be a partial solution to replacing fossil fuel energy. There is a growing awareness of the significance of this problem and a wide variety of technologies are gaining increased investment. However, the problem is hard and no technology as yet seems in sight of being both practical and affordable. The goal is $100/kWh, and/or $1/W with long life and high round trip efficiency. Most technologies exceed $500/kWh and have problems with life, efficiency and/or geography. The StratoSolar main page lists some companies trying new storage approaches in the 'related sites' list on the right.

StratoSolar PV electricity solved cost, reliability and geographic independence problems of Solar PV, but it still did not produce energy at night, and has been dependent on the eventual emergence of a viable energy storage technology. Over recent months we have made a very significant breakthrough in energy storage technology intimately tied to the StratoSolar solution. This new invention makes StratoSolar PV power plants complete 24/7 producers of electricity. The new StratoSolar technology is a variant of gravity energy storage. The most common electricity energy storage method is pumped hydroelectric, which is a form of gravity energy storage. This pumps a mass of water from a low reservoir to a high reservoir, storing energy as gravitational potential energy. Gravitational potential energy is mass times height times gravitational acceleration. For pumped hydroelectric storage, the height is small, measured in hundreds of meters and the mass is large. Measured in tens of thousands of tonnes. StratoSolar gravity energy storage instead makes use of the great height of platforms to store energy with relatively small masses. The height is about 20,000 meters, but the masses are measured in hundreds of tonnes. Winches raise the masses to store energy and lower them to recover energy. Each kg of mass can store about 54Wh of gravitational potential energy. Stored energy can scale with generated PV electricity. Each square meter of PV panel can generate about .9kWh/day to 1.3kWh/day, depending on latitude and gravity energy storage can easily store about 300Wh to 500Wh for each square meter. This balance of generation and storage allows a 24/7 electricity supply with the ability to respond to changing demand more quickly than expensive 'peaking generators'. This approach costs about $125/kWh today but with volume can scale to much lower cost. It also has a long life, high reliability and high round trip efficiency. So StratoSolar now provides a complete 24/7 replacement for fossil fuel electricity generation at lower cost and zero CO2 emissions. By Edmund Kelly The non-fossil energy from current nuclear, wind and solar are failing and will continue to fail in reducing CO2 emissions. This is borne out by all credible projections by the EIA, IEA world bank and others. Optimists in all current non-fossil energy camps rationalize why these projections are wrong, but my assessment agrees with the objective observers.

Too much of alternative energy is wishful thinking. No current choice is economically viable so the common reasoning is to pick one and argue it will get better if we support it wholeheartedly, and by implication reject the other alternatives. This makes for a polarized debate that goes nowhere. Currently the US spends about $12B/y on green energy. With current politics its hard to see this amount growing. This amount of subsidy will support wind, solar and bio at slow growth rates if they get cheaper. This is the acceptable amount of subsidy that balances the current political realities. Realistically the subsidy level is more likely to fall, with the wind PTC on a yearly cliff and the solar ITC expiring in 2016. Energy is too big a part of the economy with too many powerful entrenched interests for government to afford the subsidies or fight the battles necessary for any meaningful impact based on currently available technologies. Current economic and political realities make it clear that economically viable clean energy that does not need subsidy is the only way to grow clean energy. My point is not that we should stop supporting current non fossil fuel alternatives. What we do need to do is to invest intelligently in new non fossil technologies that might have the potential to succeed. While the debate centers on in fighting between the current alternatives, and a search for more taxes and subsidies to prop them up, a real debate on how to grow the pool of options cannot start. The air has been pulled from the room. A new approach to fund power plant development (rather than basic research) is needed. A model I like is SPACEX. This is essentially a government funded system level startup that is succeeding. Rather than the cost plus model of government contractors, this was essentially funded with fixed priced contracts for tangible results. Unfortunately the DOE has not learned from NASA's experience, and even if it had, entrenched fossil fuel interests ensure that Congress will block any attempts at reform. A stepped funding model that offered initially small funding for tangible results, with more funding as viability is demonstrated would allow a range of new ideas to be tested cheaply. There are currently a handful of fusion energy and advanced sustainable safe nuclear companies that could benefit from investments in the $10M/y to $100M/y range. There are some crazy wind and solar alternatives that might succeed. Were they to demonstrate they were on a path to viability, larger funding for the few that make it would be forthcoming. A yearly budget of $10B could fund dozens of new system level energy companies. The key would be to avoid long term subsidies for boondoggles. The $10B/y is just a swag. Less could easily accomplish a lot, and it all does not have to come from the US. By Edmund Kelly I have written previous posts pointing out the benefits of StratoSolar for Japan and the UK, two very densely populated countries with few indigenous energy sources and a desire for clean energy.

Though China is not as committed to clean energy the potential benefits of StratoSolar for China seem even more compelling, though for different reasons. In general, solar and other renewables solve three problems: 1) Fossil fuels are a finite resource. 2) Burning fossil fuels damages the environment and is causing climate change. 3) Energy security. Dependence on imported energy threatens national and economic security. Interestingly, for the US, none of these problems are currently regarded as particularly serious, and the environmental argument 2) is the only one propping up alternative energy. China is the inverse of the US. For China 1) and 3) are already a problem today, and at China's rapid rate of economic growth the problem is only getting worse. China is now the world's biggest oil importer, but its oil consumption is set to a least triple by 2040, 75% of which will be imports. This puts the Chinese economy at huge risk from oil price volatility and/or supply constraints. China has a lot of coal so coal is not in as precarious a situation, but China currently imports a lot of coal from Indonesia and Australia. An unlimited local source of cheap energy solves these problems. Not only does it remove the resource and security problem, it also potentially provides an economic competitive advantage. China has leveraged cheap coal energy into dominance of energy intensive industries like steel, aluminum and chemicals. If StratoSolar provides cheaper energy it can continue that strategy, with the added benefit of no pollution. It also puts China in a leadership position in a technology of world significance. Following the PV cost reduction path and investing in fuel synthesis technology could cement and enhance this leadership position. A quick short term benefit is StratoSolar deployment in China would help some specific industries that China has overbuilt; aluminum and PV silicon. StratoSolar systems consume a lot of aluminum for the structure, and clearly use PV panels. StratoSolar systems deployed on a large scale would rapidly become the world's biggest aluminum and PV consumer. Food for thought. By Edmund Kelly |

Archives

December 2023

Categories

All

|

RSS Feed

RSS Feed

|

© 2024 StratoSolar Inc. All rights reserved.

|

Contact Us

|