|

In june 2013 I published a blog post that contained a video focused on how to reduce world CO2 emissions from fossil fuels to zero by 2050. There has been a lot of publicity recently prompted by the release of the latest IPCC report on global warming. The IPCC keeps ratcheting up the pressure from the constantly accumulating evidence for the damage of climate change both today and projected forward into the increasingly near future. This focus at the end of another year seems a good time to revisit the primary motivation for Stratosolar. The central theme of Stratosolar is that the only viable solution to CO2 emissions reduction is clean energy that is a complete 100% replacement for fossil fuels that is significantly cheaper. Stratosolar is such a solution and current wind and solar are not.

Back in 2013 annual CO2 emissions were about 32 Gt/y. In 2018 they have increased to about 42 Gt/y, pretty much what was predicted by business as usual. There is a lot of publicity around wind and solar, but as yet they clearly have had little effect on CO2 emissions as we continue to accelerate our march towards climate armageddon. The 2013 video sets a goal of roughly 1 TWy average yearly reduction in fossil fuels to get to zero CO2 emissions between 2020 and 2050. That is still the goal but ramping production of sufficient replacement technology by 2020 is not realistic. To meet the 2050 goal and keep temperature rise below 1.5 to 2 degrees C will need a more aggressive ramp the later we start. Despite an increasing acceptance of the reality of climate change, the cost, complexity and uncertainty of clean energy solutions means adoption is low and driven mostly by government subsidies and mandates in rich developed countries. Most growth in CO2 emissions is in countries that are not the US, Europe and China. Paradoxically the US is the only player to actually reduce emissions. This has been due to cheap gas replacing coal. Wind and solar growth barely compensate for reduced nuclear. To get a perspective, todays approximately 100 GW/y of new nameplate solar is about 25GW/y of average generation. The goal is 1TW/y of average new generation. That's a factor of 40. If we split the demand evenly between wind and solar its about a factor of 20 each. That is just the generation. It does not count the storage and backup generation to achieve 100% renewable energy which are at least as much again. Currently we are spending about $250B on wind and solar. 40 times 250 is $10T/y. That cost is about 10 times current world investment in all energy infrastructure. Costs have to reduce by a factor of ten at least to fit current world energy budgets. That level of cost reduction in the relatively short time available is highly unlikely. Stratosolar eliminates the backup costs and reduces the generation cost by more than three on average, making costs within a viable range with historic cost reduction. 2TW/y of new Stratosolar at $0.75/W is $1.5T/y which is economically compatible with current levels of investment. As the IPCC shows, we are not on a path to success and time is running out It's time to evaluate what are seen as risky alternatives like Stratosolar. By Edmund Kelly

Comments

Its interesting that the two major alternatives to fossil fuel energy (wind+ solar and nuclear) are mostly at odds with each other. In the debate, they both point out the weaknesses of the other, and to an objective outsider clearly paint a picture where neither is a viable solution. The problems with cost overruns on new nuclear plants in the US and Europe have sharpened the debate recently with Toshiba’s announcement of massive losses from its Westinghouse division. The pointers at the bottom below show three perspectives on Toshiba’s woes.

My most recent blog posts have focused on the problems with intermittent wind and solar. Nuclear clearly has its problems too. Toshiba’s and others (Areva) problems at minimum show how hard current nuclear is, without even getting to how it could be modified to be more sustainable and load follow. With reactors being shut down in Europe, the US and Japan and cost overruns leading to no new orders, nuclear is not going anywhere. China is the only country adding any significant nuclear capacity. This would seem to end what had been seen as the beginnings of a nuclear revival. Most nuclear advocacy centers on new designs to remedy problems with current reactors. Nuclear takes a long time from experimental to demonstration to production power plants. Minimally the sequence takes decades and costs billions to tens of billions of dollars. So, nuclear power and wind and solar face similar problems. Neither are viable replacements for fossil fuels and it will take significant development of new unproven technologies to make them so. Compare this with StratoSolar. Much of StratoSolar is just today's PV. The unproven parts are relatively simple engineering based on existing mass produced technologies. To follow the nuclear model, the first step is to build an experimental platform. This could be done in less than a year for a few million dollars. An experimental nuclear reactor is many years and hundreds of millions of dollars. Relative to a new nuclear reactor, StratoSolar demonstration and production platform steps are equally as fast and low cost as the experimental platform. The point is that StratoSolar is no more speculative than wind, solar and nuclear, when the development paths of each that lead to viability are objectively analyzed. The perspective that wind, solar and nuclear are all unproven and speculative is not the perspective of their advocates. Wishful thinking rules the day. Recently Bill Gates led the founding of Breakthrough Energy Ventures (BEV), a fund to invest in long term energy ventures. Given Bill Gates fondness for nuclear power, funding nuclear power is probably the focus of the fund. Given the funding required to get to production plants, its very unlikely that a private fund could raise the tens of billions required even to develop one new plant. Presumably the plan is to fund the earlier cheaper development stages and persuade governments to foot the major bills. Perhaps we can persuade BEV to fund StratoSolar? It might be high risk but its cheap and fast. Its actually a typical venture funded opportunity. By Edmund Kelly Rod Adams: reporter http://www.theenergycollective.com/rodadams/2398838/toshiba-announces-6-3b-writedown-229m-construction-company-acquisition Jim Green: Friends of the earth: http://www.theenergycollective.com/energy-post/2399091/nuclear-safety-undermines-nuclear-economics Michael Schellenberger: The breakthrough institute http://www.theenergycollective.com/shellenberger/2398737/nuclear-industry-must-change-die PV is not a free market. It is dominated by China and the peculiarities of the Chinese economy. China is both the largest manufacturer and the largest consumer of PV. This has all occurred extremely rapidly over about the last five years. 2017 appears to potentially be a year of reckoning for PV, as this blog article neatly summarizes. The total historical PV cumulative installed capacity is about 300GW, most of it installed over the last few years. 2016 Installed capacity alone was about 70GW, with about 30GW of that in China. US installed a record 12GW in 2016, driven by the potential expiration of subsidy incentives. Most projections have 2017 world PV installations falling well below the 2016 70GW due to reductions in China and the US, with no major new growth area to compensate.

These reductions stem in part from the limited ability of electricity grids to absorb PV. The long-term limit is based on the capacity factor limit of grids to absorb intermittent sources. We are far from this limit, but short term constraints are showing up at very low levels of PV penetration. China’s current limit is the lack of long distance transmission capacity to take the power from the deserts in the west to the users in the east. As discussed in this blog post, California is hitting problems due to the inability of fossil generation to ramp up and down quickly enough to compensate for rapidly changing PV generation as the sun sets. Advocates for PV are focused on the falling cost of PV generation and seem to assume that once PV becomes the lowest cost of generation the world will magically switch to solar energy. The reality is far from this rosy scenario. The real cost of PV electricity will increasingly have to factor in the additional costs needed to incorporate it into the electricity supply system. California is showing the need for storage at very low levels of penetration and China is showing the need for long distance HV-transmission. Both technologies are expensive and in need of development, particularly electricity storage. They are both additions to the current grid and both exceed the cost of PV generation. Add to this the geographical variability of solar, particularly at northern latitudes and the economic case for solar to be a large scale, economically viable supplier of electricity is far in the future. StratoSolar is low cost generation with low cost, fast response storage built in and no need for long distance transmission. It has no daytime intermittency problem and it works well at northern latitudes. It needs relatively minor short term development to prove its viability. In contrast, the storage and HVDC transmission technologies needed to make ground PV viable are in many ways more speculative, unproven and longer term than StratoSolar. By Edmund Kelly Large new supplies of Helium have recently been discovered by employing modern exploration tools. This discovery may be the tip of the iceberg. There is considerable potential for discovering a lot more. This could have positive implications for StratoSolar as it raises the possibility of using Helium rather than Hydrogen as the buoyancy gas for large scale platforms. There is a lot of concern about the safety of Hydrogen and the use of Helium is a simple fix. As discussed in a question in this FAQ, current world Helium supplies are too limited for large scale deployment of StratoSolar platforms and the cost is already prohibitive. Hydrogen is a viable buoyancy gas that can be safely used with proper attention to safety engineering. However, the image of the burning Hindenburg still banishes Hydrogen from consideration. Abundant Helium resolves this issue and significantly simplifies the engineering of StratoSolar platforms.

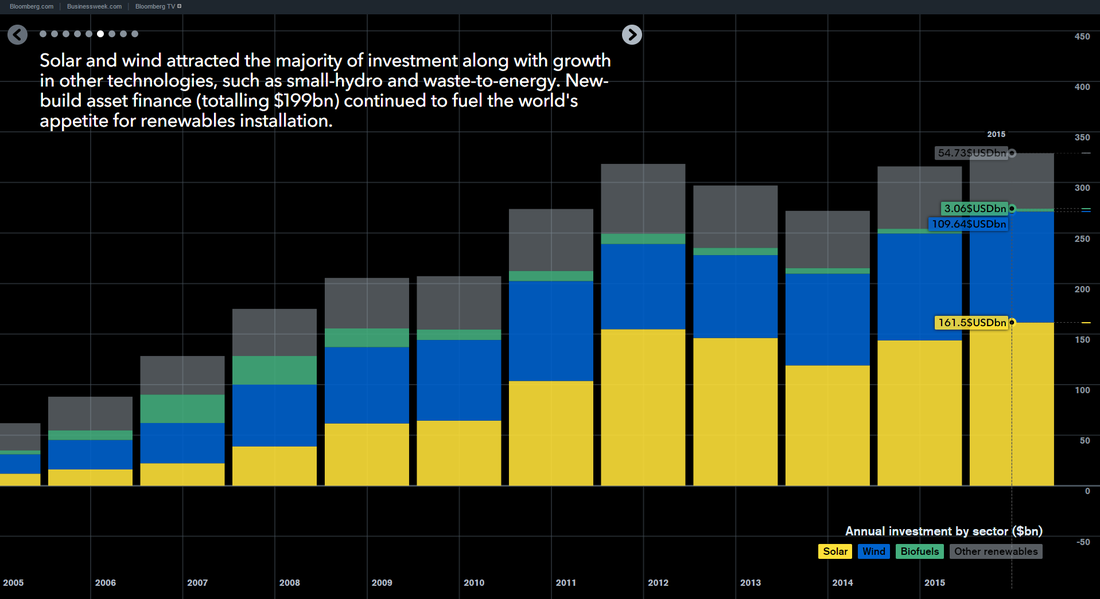

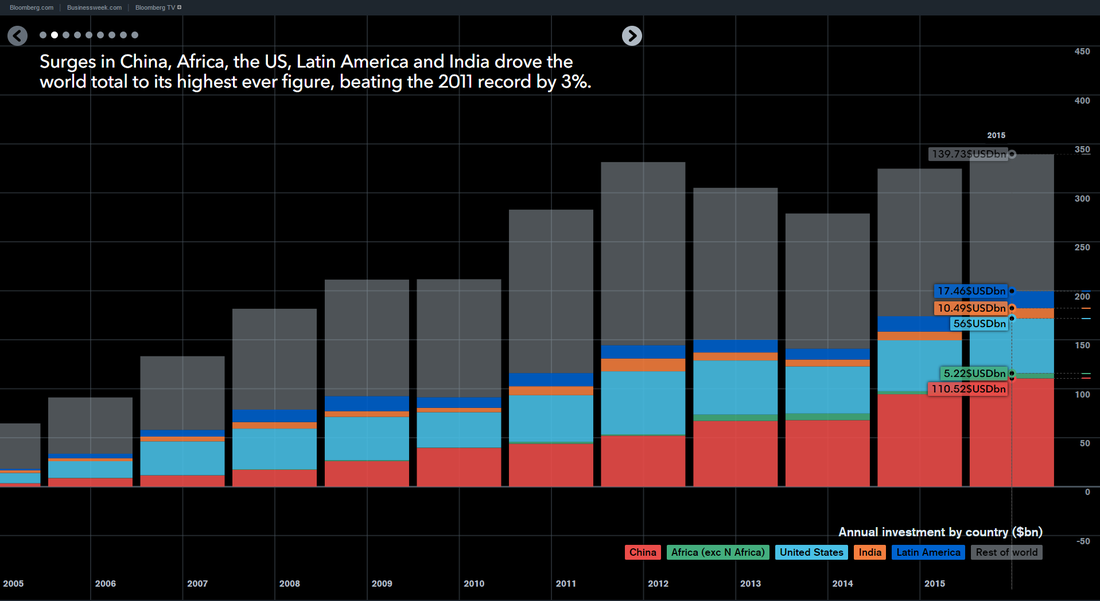

By Edmund Kelly   Bloomberg came out with a 2015 update to their report on world investment in clean energy. Above are a couple of charts showing the overall investment by type and by region. Total investment rose slightly (3%) over 2014 to $328B of which $161.5B or 50% went to solar. The overall investment level has not changed significantly for the five years, 2011 to 2015. Over this period solar has stayed about the same percentage of clean energy investment. Annual solar capacity has grown from 25GW to over 50GW, so the average cost of solar has dropped significantly from about $6.40/W($161/25) to $3.20/W($161/50), moving solar closer to wind in cost. PV panel costs have not declined much over this period ( after a dramatic decline around 2011) so most of the solar cost reduction has been from the rest of the system. The rate of these system cost reductions is slowing. The overall world average cost covers a very wide range of systems, from high cost rooftops over $6.00/W to very large utility arrays at less than $1.50/W, along with large regional differences in labour and regulatory costs. As the regional market chart shows, there has been a significant change in where the investments are taking place over the five years. The two biggest trends were the decline of Europe and the rise of China. Without China’s decision to dramatically increase its clean energy investment in 2014 and 2015, the overall market would have declined every year from 2011. Despite dramatic reductions in price, investment in solar has hardly increased. This tells us that solar investment is not yet driven by market forces. The price will have to fall substantially from current levels for solar to become market competitive. Overall the charts present a picture of a stagnant clean energy market. Given the need for government support to maintain the market, the world economic slowdown does not bode well for growth in the clean energy market, particularly in China. Despite its greater than $300B/y size, the current clean energy market is not reducing CO2 emissions by any noticeable amount. Based on these charts it is not on a path to do any better. There is a need for a change. StratoSolar makes today's PV a practical replacement for fossil fuels. Its an incremental improvement of PV, not a dramatic revolutionary new technology. It is easy, quick and cheap to prove its viability. The path we are on is clearly not working. It is worth giving StratoSolar a try. By Edmund Kelly The attached white paper is a more comprehensive look at the impact of higher energy costs on reducing GDP growth. This tells us two things. First, we are in serious economic trouble already with a low and declining rate of economic growth from the continually increasing cost of fossil fuels. Second, replacing fossil fuels with more expensive alternative energy sources will only make the problem worse. So far, wind and solar have been a relatively small economic factor, but growth to a level where they can contribute to a significant reduction in CO2 emissions would quickly get us into economic decline, and the political unrest that comes with economic decline. StratoSolar's lower cost of energy production than fossil fuels can reverse the current decline in the rate of economic growth by making energy cheaper on a continuing basis. By Edmund Kelly

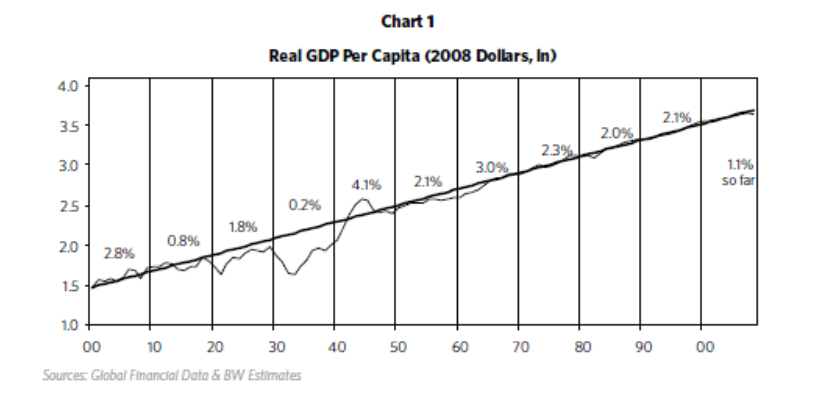

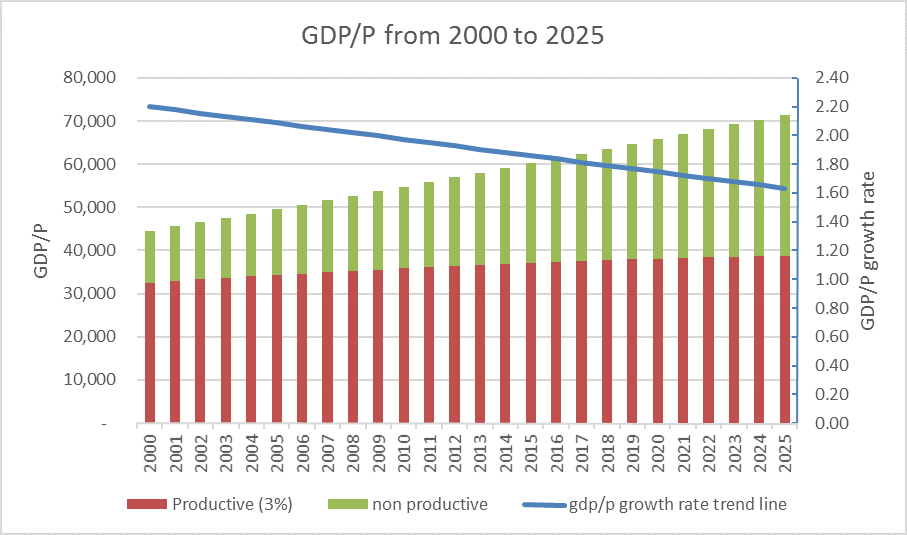

An argument against large scale deployment of alternative energy is the negative impact of the higher cost on gdp growth. The following is an attempt to quantify this effect based on the increasing cost of energy since around 1970. The modern world is based on sustained economic growth. As the chart below shows, US real gdp per capita has maintained an overall 2% per annum growth rate through depression, recessions and two world wars. This has been possible because of technological advances increasing the productivity of all economic sectors. Since around 1970, the cost of producing energy has steadily risen. Initially this was driven by the increasing cost of oil production, and more recently the cost of expensive alternative energy production has also become a significant factor. Energy is a significant part of gdp, so its share growing from around 5% to around 10% of gdp should clearly have been a drag on the growth rate of gdp, reducing it from its long term 2% per annum historical trend.  When we examine US GDP growth rate data for various periods from 1960 to today, regardless of the period chosen it is apparent that growth rates have been on a steadily declining trend. The straight line in the graph below shows a snapshot of the actual downward trend from 2000 to 2015 projected forward to 2025. The colored bars also illustrate a simple model that assumes the economy has two sectors. One sector has a high productivity growth rate of 3% and the other sector is stalled out with 0% productivity growth rate. To make the numbers fit the data we need to start with the non productive sector at 25% of GDP. This produces a breakdown like that shown, with the non productive sector continually increasing as the overall growth rate declines. These numbers imply that a larger sector of the economy than just energy is contributing to the recent decline in economic growth rate. Increased energy costs account for about a third of the decline by 2015. The other likely contributors to low growth rate are substantial parts of the financial sector, health care and education. This reduced rate of overall economic growth is causing severe economic problems already, with income inequality and stagnant wages. The problems will only get worse if the growth rate continues on its current downward trend. This illustrates that economic growth is a sensitive thing that cannot survive a large part of the economy becoming less productive. This should make it clear that a competitive, lower cost source of clean energy is a necessary condition for an energy transition that does not destroy economic growth. Current wind and solar are currently several times the needed lower cost and are reducing in cost at too low a rate to be an affordable solution for a long, long time. Other approaches like StratoSolar that can solve the problem without destroying the economy deserve some serious attention.

This white paper covers the topic of the reduction in economic growth caused by the increasing cost of energy.

By Edmund Kelly The UN climate change conference in Paris starting today (Monday 11/30/2015) has focused attention on the CO2 emissions issue The politics is focused on what can be achieved politically, which is non binding commitments to reduce CO2 without specifics on how this will be accomplished. The conference has also prompted many articles and initiatives trying to leverage the publicity associated with the conference.

There are two related items that were specifically noteworthy. To coincide with the conference The Economist magazine has just published a 16 page report on climate change. This is a factual and pragmatic overview of the problem, the potential harm and the various approaches to solutions. The report summarizes the ineffectiveness of current subsidy policies, recognizes the political unlikelihood of a world carbon tax regime, and ends by advocating more investment in R&D. Also to coincide with the conference Bill Gates announced a grand coalition pledging $B to R&D in energy innovation. The breakthrough energy coalition is a collection of VCs, entrepreneurs and tech titans. Its not clear how much money is involved or how it will be spent. It may be good news for innovations like StratoSolar, though many of those in the coalition have rejected the idea in the past. Either way the beginnings of a broader focus on energy R&D is welcome. by Edmund Kelly Bill Gates is perhaps the most influential public advocate for a "technology led" approach to reducing Green House Gas (GHG) emissions. This article, and this site are strong advocates of the "Policy led" approach. Unfortunately, as this article shows, Bill, by advocating that the funds currently used to support the "Policy led" approach be used instead to fund R&D and the "Technology led" approach is adding to the extreme polarization that marks this debate. Those who agree on the urgent need to reduce GHG emissions don't need to waste their time fighting each other. They need to talk to each other and not at each other.

A reasonable analysis would say that both approaches are necessary. It is clear that on the current path, the technologies supported by the policy led approach are not succeeding in reducing overall CO2 emissions and are unlikely to ever have a sufficiently large impact. At a global level, the developing world, which accounts for almost all growth in world energy consumption, has resisted policies to reduce GHG emissions since the 90's and continue to do so, based largely on economic concerns. When viewed at a global level, alternative energy has gone through a series of local boom and bust cycles as policy support has waxed and waned. Currently, Europe which used to be the leader has slipped back as policy has waned and China and Japan have come forward as policy has waxed. The US has gone up and down as policy has oscillated but has not been a significant player at the global level for decades. Because of declining PV prices driven by China, the Investment Tax Credit (ITC) and low interest rates have made PV investable in the US. The ITC and the US PV boom will probably end next year, a reminder of the fickle "boom and bust" nature of the "policy driven" approach. The subsidy level for alternative energy investment worldwide is about $100B/year, about half of the $200B/year world investment in alternative energy electricity generation, which in turn is about half of the $400B/year investment in electricity generation. It is going to have a hard time increasing significantly from this already significant level. We need better clean energy technologies, but as Bill Gates points out, the investment level in energy R&D is pitifully low. The "policy led" advocates have to accept this reality. "Policy led" has to accept a change to include significant R&D in a wider range of speculative technologies, not just subsidizing an entrenched status quo. By Edmund Kelly By Edmund Kelly

The rapid drop in PV panel prices in 2011 has led some optimists to predict continuing rapid price declines, particularly in the US. The triggering event in panel price decline was the drop in the cost of poly-silicon from over $100/kg to under $20/kg. This drop in price came as a result of investment in poly-silicon capacity which broke a cartel that had been keeping prices artificially high. This article by Matthias Grossmann describes the history in detail and focuses on the conditions necessary for renewed investment in poly-silicon production. He concludes that poly-silicon prices higher than the current $20/kg will be necessary to get investors on board. As supply is coming into balance with demand, that increased price is already happening, so investment in poly silicon production is likely to resume. All this means is that rapid PV panel price declines from current levels are not likely and current price levels will prevail for some time. Current overall capital costs for large utility arrays varies from about $1.50/W to $2.00/W depending on a variety of project specific details, like local labor rates, land and regulatory costs. Interestingly, if low cost financing is available and you have the high capacity factor of a desert, this capital cost level can produce electricity competitive with fossil fuels without subsidy, as is illustrated by this project in Dubai. However 100% project financing at 4% for 27 years is not yet the norm. For StratoSolar financing we assume a working cost of capital of 8.5% over 20 years which results in about $0.06/kWh for electricity. At 4% financing we would be under $0.03/kWh. That is so low a cost for electricity that it would be immediately disruptive in all markets and would drive very rapid growth in installed capacity. This would drive down costs which would further drive down the cost of electricity. If we can prove the viability of high altitude, buoyant, tethered, platforms, the foundations laid by PV growth and the continuing improvement in PV technology will enable spectacular rapid growth for StratoSolar systems worldwide. |

Archives

December 2023

Categories

All

|

||||

RSS Feed

RSS Feed

|

© 2024 StratoSolar Inc. All rights reserved.

|

Contact Us

|