Bloomberg’s latest 2023 data for PV.

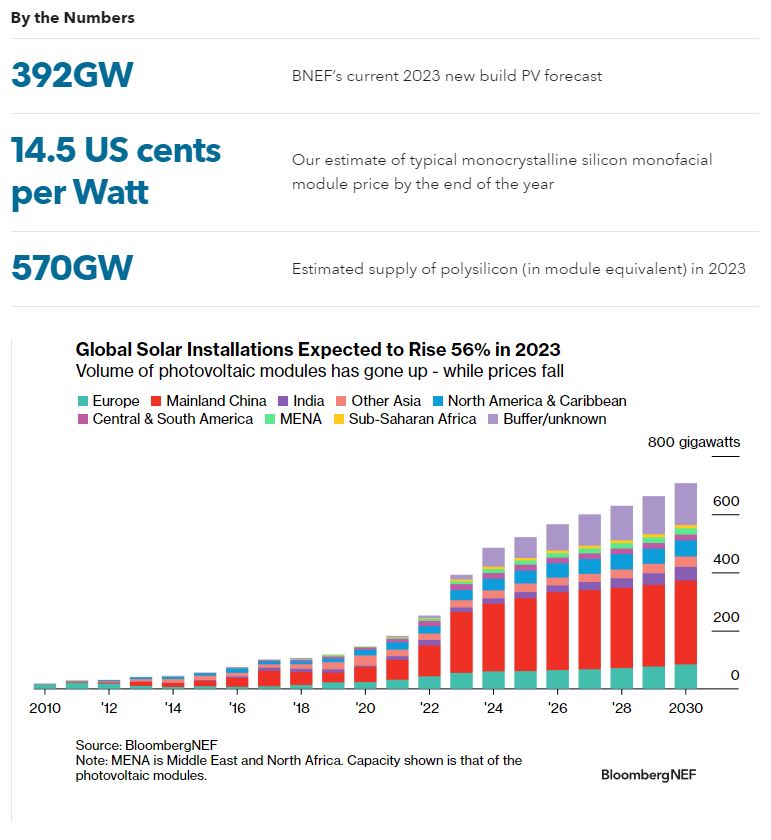

This graph shows a sudden large jump in global PV growth for 2023 from 2022, which itself was a big growth from 2021. Nearly all this new growth is from China. From the graph, China’s 2023 installations are projected at around 210GW (around ten times the US). If this rate is sustained to 2030 as shown, this will be over a cumulative 2 TW between 2023 and 2030. This graph is for DC nameplate gigawatts. PV has a lower capacity factor than fossil fuel plants so this is more equivalent to 1TW of equivalent fossil fuel generating nameplate capacity. China’s current total nameplate electricity generating capacity is less than 2TW. This would put solar alone at about 50% of total generating capacity by 2030. China currently backs up solar and wind with coal. The ability to add solar backed up by coal will stop long before this 2030 projection. To manage this level of solar will require very significant electricity storage, on the order of hundreds of GW. China is investing heavily in battery manufacturing capacity so this may end up working out. China has clearly made a strategic choice to try and reduce its dependence on fossil fuels, particularly oil where it is totally dependent on imports. It controls about 90% of global PV panel manufacturing capacity, all of which is contained within China. They have also made massive commitments to long distance HVDC transmission and have much reduced regulatory impediments. The US is vocal about the clean energy transition, but the reality is that over the last decade China invested in renewables while the US invested a lot more $T in Fracking and fossil fuels. If China maintains this projection, Its electricity could end up very low in fossil fuel consumption by 2030. It will also be much more energy secure, which is probably the main incentive. Europe and the US are on much slower and erratic energy transition timetables. By Edmund Kelly

Comments

|

Archives

December 2023

Categories

All

|

RSS Feed

RSS Feed

|

© 2024 StratoSolar Inc. All rights reserved.

|

Contact Us

|