|

Alternative energy exists solely because of a political will to make it so. It has been uneconomic from its modern inception in the 1970's, driven by the first oil crises. As a result, market driven economic viability has never been a central part of the alternative energy mindset. At its core it has been driven by two perceptions. The first was simply the need for a clean fossil fuel replacement largely regardless of cost. The second was that given time, costs would reduce to make them more acceptable.

The political will influenced government to provide subsidies to nurture the business. These subsidies now exceed $100B/y of investment worldwide and prop up a total investment of about $250B/y. However a business that depends so heavily on government support is subject to all the problems of such reliance. Firstly government support is volatile, driven by who wins elections. Secondly, subsidized industries are notoriously inefficient. Any long term subsidy regime encourages business that live off the subsidies with little or no incentive to improve. The perception that costs would reduce has been borne out by time, but the path has been a rocky one. The recent history of PV shows the erratic nature of this progress. On a day to day basis no one sees the big picture. When PV prices were stable for a decade, the perception was of stagnation which led to betting on thin film PV. When prices were falling the perception was they would continue to fall, regardless of fundamentals. Also, market size of a heavily subsidized industry is not perceived as inextricably tied to the size of subsidy. If government continues to support the PV business, costs will decline to a point where PV is competitive for some fraction of energy for sunny locations, but to be a complete solution other technologies like long distance transmission and storage have to become economically viable as well. The current rate of improvement put that point out beyond 2050. This is the status quo. Governments willing to provide limited subsidy, a business happy to live of this subsidy with its current size and rate of growth and an alternative energy political consensus that thinks this is actually working. This status quo is not reducing CO2 emissions and will not reduce CO2 emissions out to 2050. Realists point out that change of the degree necessary to reduce CO2 takes many decades and huge political will. While alternative energy imposes large new costs, the current small political will for change is directly measured by the small amount we are collectively willing to pay for subsidies. The only way to increase the political will is to reduce the cost at a faster rate or better yet turn things around and make clean energy an economic benefit. This perception is sadly lacking. The optimists place their hope in technological breakthroughs, and so we get daily updates on basic research, most of which we know will go nowhere, but create the illusion of progress. The sad reality is that basic research takes decades to make it from the lab to the market and decades more to achieve large scale. To scale quickly a technology needs both a long gestation to viability and to be mass producible. PV has recently demonstrated that it is at this point. The rapid scalability has surprised governments that provided subsidies assuming a slower ability to scale. Germany spent over $150B in two years for about 15GW before they adjusted. China just ramped to over 12GW in one year from a standing start for a lot less. So PV technology is at a point where we can make and deploy as much as we can afford. The problem is the high cost of the resulting electricity, especially if you count the costs of intermittency and storage, is just too much money for economies to sustain. StratoSolar is only PV in a new location. It reduces the cost of resulting PV electricity to market competitive levels and increases the reliability of the supply. There is no new technology or resource that limits its ability to scale. If it is proven viable, the major thing that needs to scale is PV manufacturing, the thing that has already demonstrated scalability. This is a lot like computers in the late 1980s. A large CMOS semiconductor manufacturing business had matured and companies like Sun Microsystems that built computers based on this technology rapidly scaled to volume in the millions. This pattern repeated itself for PCs in the 10s to 100s of millions and recently for mobile phones in the billions, as the cost of computers reduced with volume over time. The common elements are ability to scale supply and an affordable product with sufficient demand to match the supply. From an investment perspective the risk is like betting on a Sun Microsystems. They had engineering and market risk, but they were fundamentally enabled by available semiconductor technology. They were small investments in small teams that integrated existing technologies to build new products for very large new businesses. The market demand they produced could be met by the scalable semiconductor supply. Similarly, StratoSolar can create a demand that can be met by a scalable PV semiconductor supply. It’s continuing the triumph of the semiconductor age. by Edmund Kelly

Comments

This is the Solve For <X> hosted hangout on air for StratoSolar video recording with the addition of pictures when referenced in the discussion. The length of the video and the dialogue is unaltered.

On Tuesday Jan 14th, between 10:00 and 10:30am PST, Solve for X is hosting a google+ hangout on air for StratoSolar. It's a hosted event where I'm asked a series of questions by a moderator and the audience can also ask questions. I have never done anything like this so I'm not really sure how it will work, but people can watch and participate live and there ends up being a YouTube recording of the event.

The link https://plus.google.com/u/0/events/cv1m6fasvccse8uvlnlk9n0gf4g is to sign up to attend the hangout, post questions ahead of time, and watch it when it happens on the 14th Another way to ask questions during the event would be to tweet me at @edkellyus It's an interesting experiment. Please sign up if you can and let others that might be interested know as well. Also, as I mentioned previously, the StratoSolar solve for x moonshot video has got high ratings on the solve for x site. If you login you can rate the video in various ways. If you have not done this already, please do. https://www.solveforx.com/moonshots/stratosolar-edmund-kelly Edmund Kelly The holy grail of alternative energy is practical, affordable energy storage. Without this, wind and solar energy can only be a partial solution to replacing fossil fuel energy. There is a growing awareness of the significance of this problem and a wide variety of technologies are gaining increased investment. However, the problem is hard and no technology as yet seems in sight of being both practical and affordable. The goal is $100/kWh, and/or $1/W with long life and high round trip efficiency. Most technologies exceed $500/kWh and have problems with life, efficiency and/or geography. The StratoSolar main page lists some companies trying new storage approaches in the 'related sites' list on the right.

StratoSolar PV electricity solved cost, reliability and geographic independence problems of Solar PV, but it still did not produce energy at night, and has been dependent on the eventual emergence of a viable energy storage technology. Over recent months we have made a very significant breakthrough in energy storage technology intimately tied to the StratoSolar solution. This new invention makes StratoSolar PV power plants complete 24/7 producers of electricity. The new StratoSolar technology is a variant of gravity energy storage. The most common electricity energy storage method is pumped hydroelectric, which is a form of gravity energy storage. This pumps a mass of water from a low reservoir to a high reservoir, storing energy as gravitational potential energy. Gravitational potential energy is mass times height times gravitational acceleration. For pumped hydroelectric storage, the height is small, measured in hundreds of meters and the mass is large. Measured in tens of thousands of tonnes. StratoSolar gravity energy storage instead makes use of the great height of platforms to store energy with relatively small masses. The height is about 20,000 meters, but the masses are measured in hundreds of tonnes. Winches raise the masses to store energy and lower them to recover energy. Each kg of mass can store about 54Wh of gravitational potential energy. Stored energy can scale with generated PV electricity. Each square meter of PV panel can generate about .9kWh/day to 1.3kWh/day, depending on latitude and gravity energy storage can easily store about 300Wh to 500Wh for each square meter. This balance of generation and storage allows a 24/7 electricity supply with the ability to respond to changing demand more quickly than expensive 'peaking generators'. This approach costs about $125/kWh today but with volume can scale to much lower cost. It also has a long life, high reliability and high round trip efficiency. So StratoSolar now provides a complete 24/7 replacement for fossil fuel electricity generation at lower cost and zero CO2 emissions. By Edmund Kelly Just a brief post that backs up previous posts on PV prices ticking up as the market stabilizes. This link is about GTM's near term PV price predictions. GTM publishes market research on the PV business. They are usually bullish and over optimistic.

This is good news for the PV business, as it means that it is finally getting to a more healthy footing after several years of disarray. This is mostly because China decided to support it's PV investments by subsidizing local demand within China. It will be interesting to see how far this goes, and also it will be interesting to see how long the recent surge in Japan lasts, now that they are adopting far more limited and realistically achievable CO2 emissions reduction goals. The deeper reality is that PV panels at these prices produce electricity that is still too expensive without subsidy in almost all markets. What is called grid parity for rooftop solar is now achievable in a few markets, but this is only because retail electricity is an overpriced monopoly in those markets. Solar with current subsidy levels is a stable business, but its not likely to grow to a size that will have an impact on CO2 emissions reduction. Hopefully the failure of over optimistic projections of PV price reductions based on short term extrapolations will sober up the eternal optimists and get some sense back into discussions of viable and realistic ways to reduce CO2 emissions. I doubt it. Published By Edmund Kelly World energy use is rising with GDP growth, mostly in China and other rapidly developing economies.

Most of this energy comes from burning fossil fuels. There is a well agreed political goal to try to limit CO2 to 450ppm to limit the risks of climate change. Today the OECD consumes a little more than half of world energy (71,480TWh). By 2050, OECD countries are projected to consume little more than today (92,380TWh), but non OECD countries are projected to consume more than twice as much as OECD countries (198,526TWh). Most of this growth in energy consumption will be driven by economic growth in non OECD countries. Most of this energy will come from burning fossil fuels. Non fossil fuel energy supply, particularly wind and solar is projected to grow substantially from (21,392TWh) today to (70,703TWh) by 2050, but will only account for about 25% of all energy in 2050. The problem is the higher cost of alternative energy competes with economic growth. If you are poor, economic growth is far more important. The only rational solution to this conundrum is to find a source of alternative energy that is cheaper than fossil fuel energy. This allows economic growth while reducing CO2. The fundamentals driving these IEA projections are economic. Alternative energy from wind and solar is not market competitive, nor expected to be for the foreseeable future, so its market size is driven by the scale of government subsidies and taxes. Because of competing national objectives, world agreement is not possible, so alternative energy grows based on political will in individual nations. This will, as with all things political is very fickle. The IEA projections assume that fossil energy supply will grow to meet demand, and CO2 reduction will remain a low priority. The known supplies of coal and gas will likely meet projected demand. Oil is more problematic. Oil demand already regularly exceeds supply and given economic growth, fuel efficiency will have to improve at a rapid rate to keep supply and demand in balance. Looking objectively at these numbers a few things are pretty apparent. 1) Long before 2050 the world will face a CO2 crunch 2) An oil crunch driven by demand constantly exceeding supply is highly likely. 3) What OECD countries do will hardly matter. The non OECD countries will be the major CO2 emitters and oil consumers. These oil and CO2 crunches are big sources of potential conflict. The oil crunch will increase the cost of oil. This will reduce economic growth. As the CO2 affects become more obvious and more difficult to deny, the demarcation line will be more between OECD and non OECD countries, rather than within OECD countries as at present. As stated earlier , the only rational way to avoid these looming conflicts is to find a CO2 free energy source that is cheaper than fossil fuels. This removes clean energy as an impediment to economic growth. Instead it has the opposite effect. It enhances economic growth. This is the point where as usual I plug StratoSolar as a clean and cheap energy source that meets all the requirements. By Edmund Kelly A simple question is why can’t ground PV do the same thing as the StratoSolar scenario? The simple answer is it is too expensive and it won’t get cheap enough anytime soon. The sharp drop in PV prices over the last few years have stopped, and there is no rational basis for them to fall further for a long time. A good thing about the recent price drops is it has raised awareness of PV and its potential for further improvement. A bad thing is it has created over optimistic and unrealistic assessments of PV’s chance to be a significant energy provider in the short term.

In the end, energy is all about politics and economics. StratoSolar PV panels have an average utilization of 40%. Ground PV panels have an average utilization of about 13%. Based on a simple analysis, ground PV electricity costs three times as much, and importantly this is significantly more than electricity costs today. That means that it can only be sold with the help of subsidies. As Germany has demonstrated, profitability drives investment. By providing subsidies that guaranteed profitable investment, German private industry jumped at the opportunity and installations grew very rapidly. Japan and China are following Germany’s lead. But things are actually worse than this. Its always tempting measure solar with the best utilization from sunny places, but unfortunately with solar its all about geography. There are very few places with good solar near population centers. Southern California is a rare example. Take Germany as a more representative example. PV utilization in Germany is around 11% from the published data. Germany could do a deal with a sunny location and build HV transmission lines to transport the power. This has numerous problems. On purely money terms, as panels have reduced in cost, and transmission lines have not, its likely that the better PV utilization in the desert will not cover the HV transmission costs. Don’t forget that the transmission lines will have the low PV utilization, which more than doubles the cost compared to conventional HV transmission lines. On top of this are the political constraints. HV transmission lines are not liked, and the countries where the panels and HV transmission lines are placed may not be the most politically stable. Even in the US, politics and economics will favor New York, for example, building in New York rather than dealing with getting power from New Mexico via transmission lines through many states. What this means is that ground PV discriminates, and northern climes get to pay twice as much, or more for electricity. Economics will also dictate that southern climes will get most of the synthetic fuel business. Because of the lower utilization, ground PV electricity will always cost 3X StratoSolar electricity. This factor makes StratoSolar economic for electricity, and then fuels long before ground PV. The learning curve is good but not that good. The learning curve will not continue for ever, and when it slows it will create a permanent cost barrier that ground PV will never overcome. StratoSolar is far less variable with geography, so Germany or New York, for example could provide all their energy needs, both electricity and fuel, locally. So to summarize, ground PV is too far from viability today, and too variable with geography to ever be an easy political choice. StratoSolar is viable today, and does not discriminate against geography. The StratoSolar capital investment for both PV plants and synthetic fuel plants will average a sustainable $0.6T/year, in line with current world energy investment. $2T/year capital investment for ground PV is a lot harder to imagine. By Edmund Kelly Thisarticle in Renewables Energy Focus magazine provides more details on the state of the PV market as companies report their earnings. SPV Market Research puts the PV panel market in 2012 at 25GWp and $20B. Panel maker losses exceed $4B. This comes as Suntech the number six PV panel manufacturer declares bankruptcy.

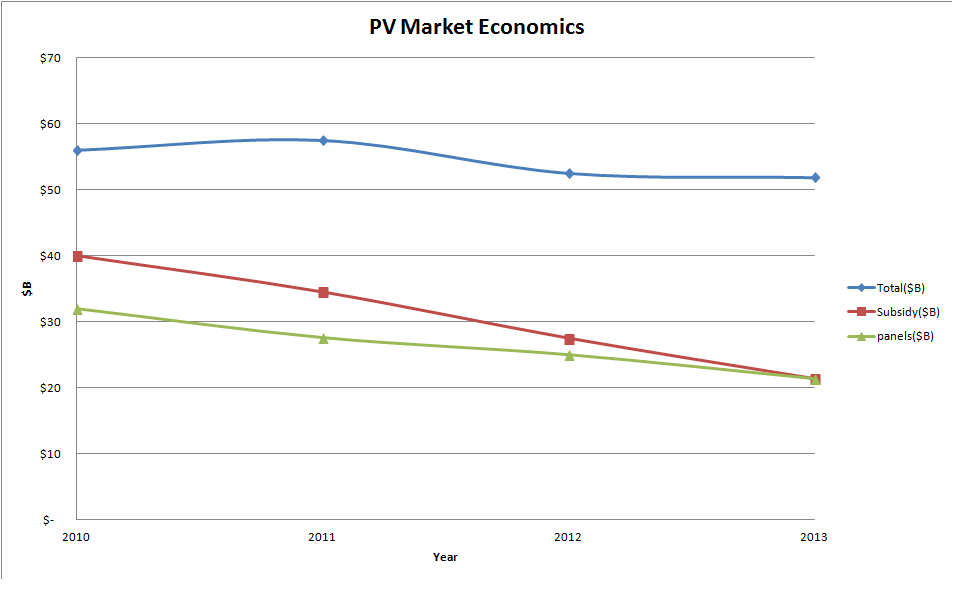

2013 is not shaping up as much better than 2012. Major shifts in regional demand are underway, driven by where the subsidies are growing or declining. European demand is shrinking with reduced subsidy, but China has a profitable FIT and a goal of 10GW, and the generous FIT in Japan is projected to see 6GW installed. The Japanese growth will be met by Japanese panel makers despite their lack of market competitiveness, which may not help the PV business generally. Current panel prices combined with subsidies are also driving growth in the US(primarily California), which may see 5GW installed in 2013. The story is the same everywhere. Subsidies drive the market, and their amount determines the market size. The overall PV market is not likely to grow significantly in 2013 over 2012. As prices stabilize, and even rise a bit to restore profitability, the historical learning curve of PV panel price versus cumulative volume is still holding up very well. This is important to understand as it establishes the realistic fundamentals that should drive expectations for what can be achieved by PV. There has been a tendency to take an optimistic view of PV competitiveness based on extrapolating short term trends, or localized successes (like Germany) driven by large subsidies. PV has made great strides, but is still only competitive with a large subsidy in normal geography, or with a smaller subsidy in a sunny geography like California. The historical learning curve will take many years of current production rates to get PV panel prices down to competitive levels. To put things in perspective, PV on a world average has less than a 15% utilization. StratoSolar is 40% utilization on average. For ground PV panels to match StratoSolar, prices will have to more than halve from current levels to about $0.30/Watt. This will take a long time, perhaps decades. It’s a catch 22 for ground PV. Prices will only fall with volume, but volume will only happen with lower prices. StratoSolar competitive energy pricing has the potential to fundamentally change the energy market by driving PV volume installation now. By Edmund Kelly Analysis of the PV market in 2012 have continued to roll in. They vary considerably in their estimates of PV capacity installed, several estimating capacity installed exceeded 30GWp. A recent report from NPD Solarbuzz was less optimistic. According to the market research firm, PV demand in 2012 reached 29GW, up only 5% from 27.7 GW in 2011. Notably, the growth figure is the lowest and the first time in a decade that year-over-year market growth was below 10%..“During most of 2012, and also at the start of 2013, many in the PV industry were hoping that final PV demand figures for 2012 would exceed the 30GW level,†explained Michael Barker, Senior Analyst at NPD Solarbuzz..“Estimates during 2012 often exceeded 35GW as PV companies looked for positive signs that the supply/demand imbalance was being corrected and profit levels would be restored quickly. Ultimately, PV demand during 2012 fell well short of the 30GW mark.†As usual, the industry and analyst projections going forward are for things to improve dramatically. A more sober analysis would say that the market will continue its painful restructuring with slow to modest growth. The analyses tend to focus on GW installed but a look at the dollar numbers is more revealing of the state of the industry and its likely future.  This graph shows a simple analysis of relevant dollar numbers rather than GW installed numbers for 2010, 2011,2012 and an estimate for 2013 based on a forecast of an increase of 20% in GW installed, which may be optimistic.

The Total line shows the total world dollars spent on PV systems, which includes PV panels and Bulk of Systems (BOS). This line has been relatively constant at between $50B and $60B. Over this timeframe the combined reduction in panel and BOS costs has offset the decline in subsidy. The panel line shows that revenue to PV panel makers has been declining significantly. The increase in GW has not offset the fall in PV panel prices, and the revenue decline will continue in 2013. As is known the PV panel business has a capacity to produce about 60GW/year, but demand is about 30GW/year. This has led to severe industry restructuring and low panel prices that in many cases are below the cost of production. There is no new investment in capacity, so the current panel prices are unlikely to fall significantly if most manufacturers are already losing money. The subsidy line shows an estimate of the amount of total world subsidy. This, as is well known has been declining, but the decline has been dramatic. Germany alone pumped in over $100B over 2009-2011, but is now well below $10B/year. China has stepped in energetically, and there is support in Japan and the US, but it still only adds up to half of what Europe used to support, and the overall subsidy amount continues to decline. The PV business is still driven by subsidies. They have declined from about 60% to about 40% of the business, but are still necessary, as current PV systems do not make electricity at competitive costs despite the dramatic PV panel price decline. The overall net effect of panel price declines and subsidy declines has been a market with fairly constant overall revenue. If worldwide subsidies increased that would drive growth which would use up the excess panel manufacturing capacity which would lead to profit and investment in new more efficient capacity and panel price declines that would reduce the need for subsidy. If subsidies continue to decrease, there is little room for PV-panel prices to decline further, and so the overall business will shrink. None of this is coordinated at a world level, so it could go either way. The prospects for increased subsidies overall worldwide seems low, given the current economic focus on austerity in Europe and the US. This has been a long article to get to the simple conclusion that the PV business is unlikely to grow dramatically in the near future and current PV panel prices are likely to prevail for at least several years. Also, optimistic projections for PV panel price reductions based on projecting the recent dramatic drop forward are not realistic, and estimates based on the historical long term trend are likely to prove more accurate. PV at around 30GW/year installation is a tiny fraction of world electricity generation (5000TW), never mind world total energy. The only way to get a dramatic growth in PV is to either get PV to produce electricity at a cost that generates sufficient profit to attract private investment, or massively increase world subsidies. StratoSolar offers the profitable investment path. Our current design if deployed today with current PV cells would generate electricity for $0.06/kWh with very conservative platform cost estimating. This is profitable without subsidy in almost all markets. By Edmund Kelly |

Archives

December 2023

Categories

All

|

RSS Feed

RSS Feed

|

© 2024 StratoSolar Inc. All rights reserved.

|

Contact Us

|