|

By Edmund Kelly

This article provides more evidence that the optimistic hopes for rapid growth in world PV installations seem to finally be running up against the economic and practical constraints. China in 2014 is a good example. China's PV goal for 2014 was 14 GW. It now appears actual installations will be about 10 GW (as was predicted earlier). In 2013 the bulk of PV installations in China were large utility scale. In 2014 they wanted to move the bulk to rooftop installations. This was motivated by growing electricity transmission bottlenecks. Rooftop installations don't need new transmission but take longer and are considerably more expensive than large installations. So China was caught between a rock and a hard place. Utility systems mean building lots of expensive long distance transmission that takes years and has political opposition. Rooftop PV is more expensive and less efficient and is also relatively slow to install. Neither option could meet the 14 GW goal. The projections for next year are also for 10 GW. That would be three years in a row at about 10 GW. This just adds one more piece of evidence to the case that none of today's carbon free energy technologies are practical or economically viable alternatives to fossil fuels. This includes wind, solar, hydro, bio and nuclear. All require government support to survive and governments cannot afford to support any or all of them at the significantly higher level needed to displace fossil fuels. The advocates of each technology are happy to take government subsidies and keep tilting at windmills as long as government keeps providing the subsidies. There are attempts at advanced versions of wind, solar and nuclear, but investment levels are miniscule. We are spending over $250B on installing clean technologies that cannot succeed, but investing a tiny fraction of that on R&D for technologies that might succeed. This is especially true for system solutions like Nuclear or large Solar. In part its because government is bad at and should not be involved in picking winners. Finding a structure to finance large scale energy R&D has proved elusive. It would take venture investments at a considerably larger scale than current venture capital funds can support. For a portfolio approach to work a fund would need maybe $100B to invest in maybe 100 ventures over maybe a decade. Given the scale of energy, one success would be enough.

Comments

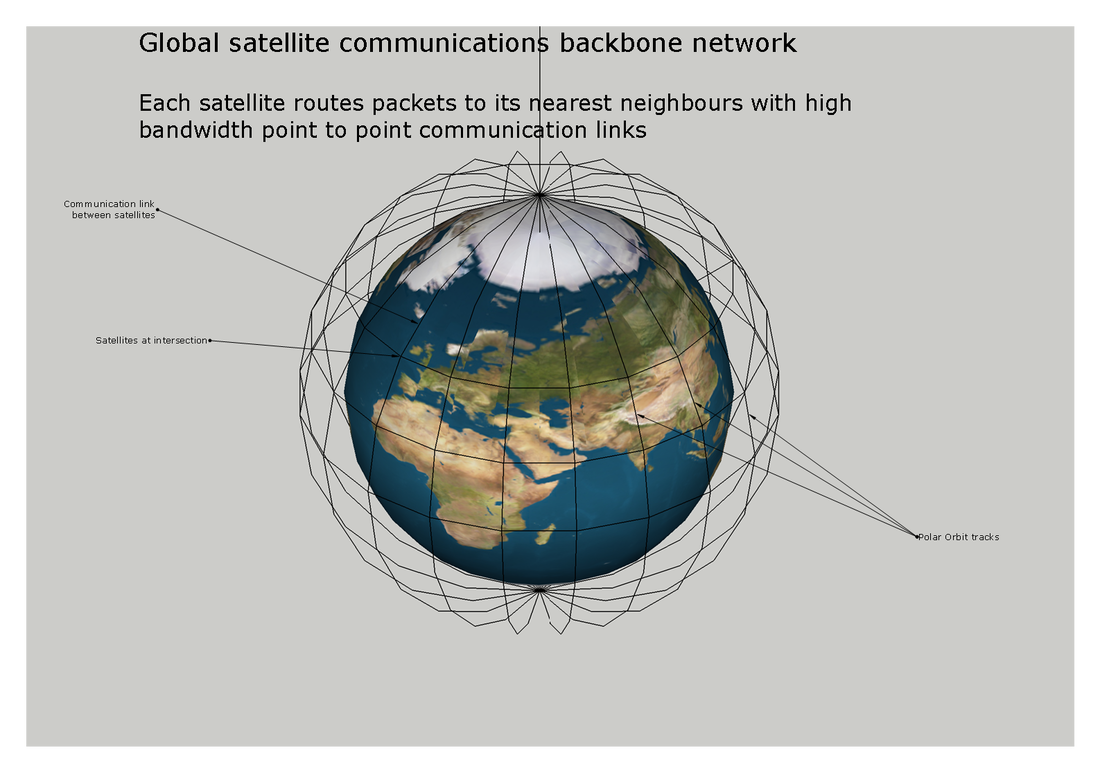

A StratoSolar platform’s unique capability to enhance emerging satellite Internet communications9/29/2014  400 satellites in polar orbits at 800km altitude. 20 orbital planes with 20 satellites in each plane. Each satellite has four nearest neighbours. Google and Facebook have both publicly announced they plan to spend billions on satellite communications to bring internet access to the developing world. Recent departures from Google of key personnel associated with Google's satellite communications effort shed some light on the reality of what is happening at Google and elsewhere. These efforts are very real and have implications far beyond internet access for the developing world.

Apparently a team that Google had hired from O3b including Greg Wyler, Brian Holz and David Bettinger have recently departed Google and are the founders of WorldVU a satellite internet start up aiming to launch 360 satellites into 800 km and 950 km polar orbits starting in 2019. WorldVU has the rights to 2 GHz of KU band (12-18 GHz). Satellites will fly in 20 planes each with 18 satellites providing complete world internet coverage. Also, Michael Tseytlin, another satellite executive previously at Google recently joined Facebook’s connectivity lab. This article implies he has some authority. While these departures imply some confusion at Google, their recent purchase of Skybox means they now have in house capability to design and deploy satellites. Skybox has made and launched small satellites for imaging. This has obvious tie ins with lots of Google mapping and geographical information efforts but this expertise could also be leveraged for telecommunications. So it appears that there are three very serious efforts to launch low earth orbit constellations of satellites for internet communications. WorldVU, Google and Facebook are publicly each spending billions on their individual efforts and the movement of the key individuals mentioned previously backs up the reality of their statements. These are the early participants in what may turn into a new wild west in space as the broader implications of this emerging technology become apparent. Obvious examples of companies with both the financial resources and business need to compete are Apple and Microsoft. The public focus of these efforts at the moment is on the satellite to ground links that provides Internet access to the developing world, but the implications of the technology are potentially far more significant than that. The point to point communication links between satellites together form a private, high bandwidth, global, secure, reliable, backbone communications network that is independent of any nation. Based on free space optical (FSO) links and/or high frequency point to point microwave links the bandwidth of this backbone in space could eventually surpass that of the terrestrial internet backbone. Nations can control communications from the satellites to the ground but not point to point communication between satellites. Discussions of satellite communication for the developing world usually focuses on the customer end but an equally important aspect is the backhaul communications to the internet backbone. Backhaul relies on high bandwidth wireless communication between satellites and complex ground stations connected to the Internet backbone. This communication needs expensive, scarce and highly regulated bandwidth and expensive and complex ground stations. This is where StratoSolar platforms can offer a unique capability not possible with Loon, drones or High Altitude Airships. Because they are above most of the atmosphere, the same (unregulated) free space optical (FSO) links or high frequency microwave links used to communicate between satellites can communicate reliably with a receiver on a StratoSolar platform that then forwards the communications down high bandwidth fiber optic links attached to the tether. The tether is a unique attribute of StratoSolar platforms that is usually seen as a negative, but for this application it is a big positive. This connects the backbone in space directly to terrestrial backbone networks with the same private, high bandwidth, secure, reliable, communications. StratoSolar platforms can be situated near convenient connection points to the backbone or data centers. When thought of as data center connections, the ability of the platforms to also provide reliable 24/7/365 power to the data centers would allow more flexibility in data center location and less dependence on external energy infrastructure or logistics like fuel supply. This vision of an internet backbone in space seems an entirely plausible consequence of the coming low earth orbit satellite networks and the unique capabilities of the StratoSolar platform and its tether would make the case even stronger. By Edmund Kelly

Google and Facebook have raised awareness of alternative strategies to get Internet service to the other three billion (O3B) without internet access in the developing world. Their motivations are not altruistic. The O3B are their future customers. Google is pursuing balloons with the Loon project, high altitude drones with its purchase of Titan, and satellites with its announcement that it plans to deploy a constellation of 180 medium earth orbit satellites. Facebook has announced it is deploying satellites and purchased Ascenta, a drone company.

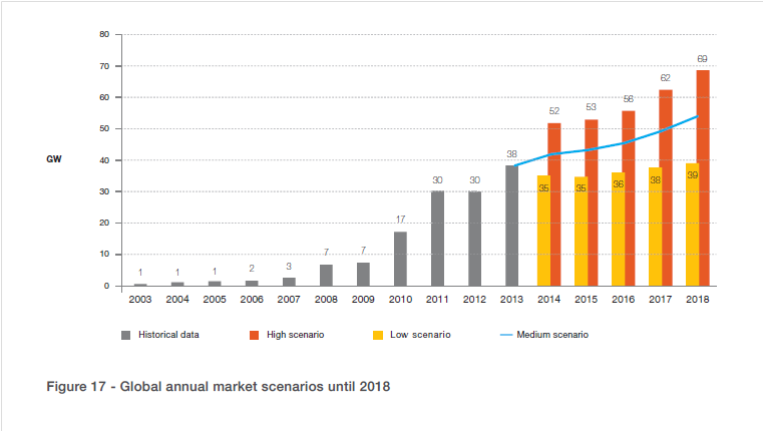

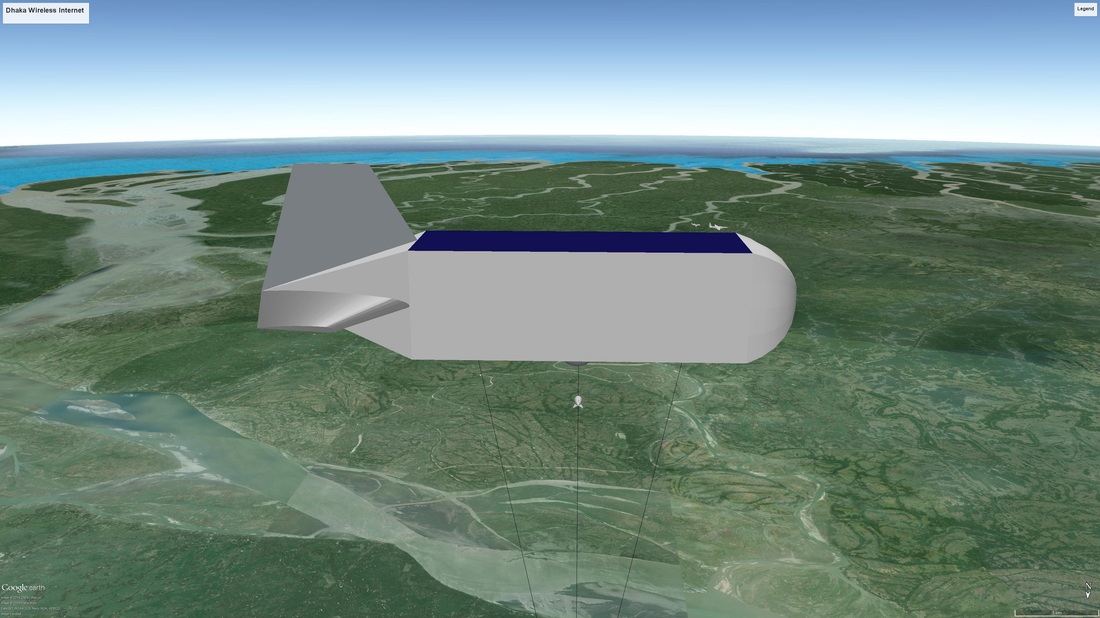

A quick look at internet statistics shows that the majority of those without an Internet connection are in Asia, about 2.8 Billion. A look at land areas in the countries that account for the bulk of the market shows that population densities are very high. This combination requires a high total bandwidth over relatively small land areas. We call this a high bandwidth density solution. Current and proposed satellite solutions can only provide low bandwidth density. Similarly Google Loon and high altitude drones have very small payloads and can only provide low bandwidth density. All these technologies are years from deployment and have difficulty with a low $1.00/month price. We propose a high bandwidth density StratoSolar platform wireless Internet solution using stratospheric permanently tethered platforms. A platform tethered at 20km altitude can provide reliable wireless internet service to a radius of about 75km, which is an area of about 15,000km2. For the population density in Asia, a wireless internet platform solution covering an area of 15,000km2 needs to provide enough bandwidth for from about 1,000,000 to 8,000,000 customers, or up to a total of about one terabit per second for broadband access. A crude analysis to scope the problem yields a platform count of about 1,100 for Asia. In most cases there are low population density areas that would be best served with low bandwidth density solutions like satellites, so the number of platforms would be less (perhaps 600). This is especially true for China. There would also be very high bandwidth density areas in urban cores where the wireless platform bandwidth density would be insufficient to satisfy the entire market. We propose a quickly deploy-able solution based on existing hardware and software currently being used by the rapidly growing wireless internet service provider (WISP) market that uses the unlicensed radio bands. As is currently done with satellites we propose to provide very large overall bandwidth by using many spot beams with massive frequency re-use. The solution can be thought of as a WISP with a very tall tower that supports a lot of antenna. With highly directional antenna at both the platform and the customer the link budgets are conservative and the interference requirements of the unlicensed bands can be met. We would envisage from about 271 to 1000 cells per platform, providing broadband Internet access to from 1,000,000 to 8,000,000 customers. The aggregate cell throughput exceeds 1Gb/s. The large payload, large antenna support structure area, and large continuous PV power with gravity energy storage provided by the platform are what enable the rapid deployment of this platform composed largely of off the shelf wireless internet and internet switch hardware. The off the shelf wireless hardware and the antenna are not designed for miniaturization and weigh several tonnes and consume several kW of power. The major impediment to deployment is political. Each country will be different. The only physical problem is the hazard that tethers pose to aviation, which can be handled by the airspace regulator of each country. Commercial aviation in Asia is very small and general aviation is almost non-existent compared to the US and Europe. The politics of communications infrastructure are harder to gauge. China may be a non starter. The initial goal is to get one country to deploy one platform. The economics are very favorable and would provide internet service at prices that most households in Asia could afford . If the average platform has 4,000,000 customers at $1:00/month, that is $48M/year income for a platform that costs about $4M including the wireless hardware. Customer premises equipment (CPE) would be about $25 or less per customer. $25 is a lot of money in large parts of the target market, so reducing CPE costs and methods of financing CPE are important. From an individual countries perspective, internet service deployment can occur without much investment and in a timeframe dictated mostly by customers. High altitude platforms will deploy in less than a week once airspace is approved. Coverage for a country could be deployed in less than a year. Initially a backbone internet could be provided with wireless or FSO links between platforms. Once a platform is deployed customers can buy or rent CPE and be on the internet immediately. They will need electricity, but that might come from a PV panel and a battery in an isolated area. A local wireless base station could provide Wi-Fi internet to a village. By Edmund Kelly This sixty page report EPIA Global Market Outlook for Photovoltaics 2014-2018 paints a pretty accurate picture of the recent history of the global PV market and has realistic projections for the near term. It has detailed information for each geography and market segment. The graph below from the report shows the near term overall world market projection with optimistic, pessimistic and realistic scenarios. The realistic middle scenario shows slow overall market growth, but no spectacular take off. The conclusion of the report is a welcome return to reality about the future prospects for PV and a marked contrast to the over optimistic assessments that still seem to pervade the PV business. The central point of the conclusion is that “ The PV market remains in most countries a policy driven market, as shown by the significant market decreases in countries where harmful and retrospective political measures have been taken.” A policy driven market is a euphemism for a subsidy driven market. This lines up with my assessments of the prospects for PV business over the last several years as published in this blog. PV growing at this rate is fine for the PV business, but will not make PV a significant source of electricity anytime soon. It is not sufficient growth to drive costs down, so the business will need subsidy for the foreseeable future. The conclusion of the report backs this assessment as it clearly states that growth is dependent on “sustainable support schemes”. i.e. more subsidies. At some point those that promote current policies in the belief that they will reduce CO2 emissions have to stand back and make a realistic assessment of what they are accomplishing, or more accurately failing to accomplish. By putting all their eggs in the current wind and solar baskets, they are actually precluding investment in possibly better technologies. The psychology seems to be driven by a fear that admitting that current wind and solar are failing, will lead to nothing being done, and something is better than nothing. The reality is that investing only in failure guarantees failure. By Edmund Kelly

In the computer industry there is the concept of “computer platforms” Examples are the PC platform, the MAC platform and the Android platform. The platforms are combinations of hardware and software that act as a standard basis for many applications. In a different more physical way, StratoSolar technology has evolved into a platform for multiple applications.

We initially developed the technology targeted at solar PV electricity generation. Doing this involved solving a series of significant problems that led us to methods for the design, construction and deployment of small to large scale modular, buoyant-platform systems. The first additional platform application beyond PV generation we serendipitously discovered was gravity energy storage. This is very synergistic with intermittent PV generation. Cost effective energy storage is an area in great demand without any clear solution today . As well as complementing PV generation for the energy market, this also means that small stand alone platforms can supply energy for other platform applications. Such an emerging application is wide area wireless internet communications. The platforms we have evolved can quickly and cheaply provide very cost effective wireless internet communications. Other more conventional broadcast and cellular communications can also easily benefit. One thing leads to another. The use of winches to store energy by transporting weights from the ground to the platform and 20km altitude also enables the transport of goods, equipment, and ultimately, people from the ground to platforms at 20km and back. This means that communications and observation equipment can be deployed and recovered without bringing platforms down to the ground. The weights involved with gravity energy storage can get to several hundred tonnes. This leads to another possible application; containerized goods transportation. At various times attempts have been made to revive the use of airships without success. Airships suffer from their fragility. Within the troposphere violent and unexpected weather can destroy airships, either in flight, or more commonly in accidents when near the ground for docking and undocking. However, large stratospheric airships based on the StratoSolar construction method could carry payloads of several hundred tonnes between platforms while remaining permanently in the stratosphere. They would be powered by fuel delivered to the platforms, perhaps augmented with solar energy during the day. Containers would be transported with winches up to a platform, transferred to a docked airship, transported by airship to another platform where the airship docks and the containers are transferred to the platform and lowered with winches to the ground. Airships would be relatively cheap to buy at around $5M, cheap to operate, and would transport goods at about 100km/h from platforms that can be positioned anywhere. The cost of transportation would be somewhere between ships and aircraft, perhaps similar to trucks, but would be point to point and relatively high speed. Transportation is currently a long shot for StratoSolar, but indicates how a technology can evolve far from its original source. Many other expected and unexpected StratoSolar platform applications will inevitably evolve. Looking at the money, for 2013, world GDP was $72T, of which energy was $6T, or about 8% of GDP. That $6T can be thought of as the income of the overall energy industry. This income balances with industry profit, investment and O&M. From IEA data the energy industry investment part was about $1.5T, of which about $0.8T was in oil and natural gas infrastructure, $0.4T was investment in electricity generation and $0.3T was investment on electricity transmission and distribution.

From Bloomberg data, investment in wind and solar generation in 2013 was about $200B, with additional clean tech investment of about $50B on smart grid, biomass and bio fuels. Some of the investment in transmission and distribution is to integrate wind and solar and some smart grid spending is also related to wind and solar integration. So current investment in clean energy generation is over half of all investment in electricity generation . I have to admit I found this surprising. I always see alternative energy as the underdog, not the biggest player. That $200B bought about 45GW ($82B) of nameplate wind and about 35GW ($114B) of nameplate solar. Using average generation as the metric, conventional power plant capacity runs on average at about 50% utilization worldwide, so the world’s almost 6TW installed capacity generates an average 3TW of power. The 45GW of new wind generates an average of about 12GW and the 35GW of new solar generates an average of about 5GW, for a total of about 17GW of new average generation. That's 17/3000 or about 0.5% of current average electricity generation. The other $200B bought about 140GW of coal, gas, hydro and Nuclear power plants, mostly in China and India, that generate more than 70GW of average power or about four times the 17GW average of the new wind and solar. When we account for the cost of fuel, wind and solar electricity averages about two to three times the cost of electricity from other sources. Most of the investment in new electricity generation is driven by economic growth which needs to add about 3% of new generation every year. If just that increase was met with current wind and solar, it would cost close to $1T/y. That does not cover replacing the existing generation. Of the $200B spent for wind and solar, government subsidies account for at least half, or $100B. This is a look at the money. The bottom line is that wind and solar are already the biggest money part of electricity generation but are not providing much electricity. To scale wind and solar up just to meet current new generation demand would mean they would probably be the biggest industry on the planet. By Edmund Kelly Alternative energy exists solely because of a political will to make it so. It has been uneconomic from its modern inception in the 1970's, driven by the first oil crises. As a result, market driven economic viability has never been a central part of the alternative energy mindset. At its core it has been driven by two perceptions. The first was simply the need for a clean fossil fuel replacement largely regardless of cost. The second was that given time, costs would reduce to make them more acceptable.

The political will influenced government to provide subsidies to nurture the business. These subsidies now exceed $100B/y of investment worldwide and prop up a total investment of about $250B/y. However a business that depends so heavily on government support is subject to all the problems of such reliance. Firstly government support is volatile, driven by who wins elections. Secondly, subsidized industries are notoriously inefficient. Any long term subsidy regime encourages business that live off the subsidies with little or no incentive to improve. The perception that costs would reduce has been borne out by time, but the path has been a rocky one. The recent history of PV shows the erratic nature of this progress. On a day to day basis no one sees the big picture. When PV prices were stable for a decade, the perception was of stagnation which led to betting on thin film PV. When prices were falling the perception was they would continue to fall, regardless of fundamentals. Also, market size of a heavily subsidized industry is not perceived as inextricably tied to the size of subsidy. If government continues to support the PV business, costs will decline to a point where PV is competitive for some fraction of energy for sunny locations, but to be a complete solution other technologies like long distance transmission and storage have to become economically viable as well. The current rate of improvement put that point out beyond 2050. This is the status quo. Governments willing to provide limited subsidy, a business happy to live of this subsidy with its current size and rate of growth and an alternative energy political consensus that thinks this is actually working. This status quo is not reducing CO2 emissions and will not reduce CO2 emissions out to 2050. Realists point out that change of the degree necessary to reduce CO2 takes many decades and huge political will. While alternative energy imposes large new costs, the current small political will for change is directly measured by the small amount we are collectively willing to pay for subsidies. The only way to increase the political will is to reduce the cost at a faster rate or better yet turn things around and make clean energy an economic benefit. This perception is sadly lacking. The optimists place their hope in technological breakthroughs, and so we get daily updates on basic research, most of which we know will go nowhere, but create the illusion of progress. The sad reality is that basic research takes decades to make it from the lab to the market and decades more to achieve large scale. To scale quickly a technology needs both a long gestation to viability and to be mass producible. PV has recently demonstrated that it is at this point. The rapid scalability has surprised governments that provided subsidies assuming a slower ability to scale. Germany spent over $150B in two years for about 15GW before they adjusted. China just ramped to over 12GW in one year from a standing start for a lot less. So PV technology is at a point where we can make and deploy as much as we can afford. The problem is the high cost of the resulting electricity, especially if you count the costs of intermittency and storage, is just too much money for economies to sustain. StratoSolar is only PV in a new location. It reduces the cost of resulting PV electricity to market competitive levels and increases the reliability of the supply. There is no new technology or resource that limits its ability to scale. If it is proven viable, the major thing that needs to scale is PV manufacturing, the thing that has already demonstrated scalability. This is a lot like computers in the late 1980s. A large CMOS semiconductor manufacturing business had matured and companies like Sun Microsystems that built computers based on this technology rapidly scaled to volume in the millions. This pattern repeated itself for PCs in the 10s to 100s of millions and recently for mobile phones in the billions, as the cost of computers reduced with volume over time. The common elements are ability to scale supply and an affordable product with sufficient demand to match the supply. From an investment perspective the risk is like betting on a Sun Microsystems. They had engineering and market risk, but they were fundamentally enabled by available semiconductor technology. They were small investments in small teams that integrated existing technologies to build new products for very large new businesses. The market demand they produced could be met by the scalable semiconductor supply. Similarly, StratoSolar can create a demand that can be met by a scalable PV semiconductor supply. It’s continuing the triumph of the semiconductor age. by Edmund Kelly

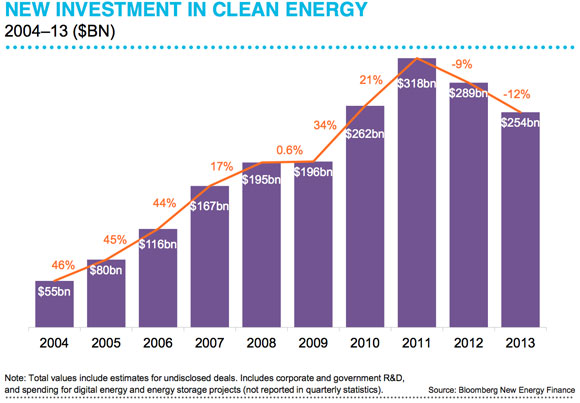

This Bloomberg graph shows world investment in clean energy declining over recent years. These declines are due to reducing government subsidies in turn reducing investment. This illustrates that government subsidies drive the market, a point that is rarely discussed, but is extremely important if you want to predict future market trends, as Bloomberg tries to do. If you read the analysis and projections, the fact that they depend almost 100% on predicting subsidies is never really stated. That’s because government actions are fickle and hard to impossible predict for timescales of years.

A bigger issue is that market size is determined by the amount of subsidy. At least one half of the clean energy investment shown is from subsidies. That is a minimum of $125B in 2013. Given that to make a significant impact on energy, we need to provide ten to one hundred times current yearly wind and solar alternative energy capacity additions, the implication is very large government subsidies of $1.25T/y to $12.5T/y. However, overall world subsidies seem set to decline further in 2014 and beyond, not grow. Europe has scaled back its clean energy agenda and the US with cheap gas is likely to reduce subsidies even more. Growth in China and India is slowing. Wind and solar power generation costs may reduce, but transmission, storage and other infrastructure costs will easily make up for this. None of this bodes well for reducing CO2 for the foreseeable future. The only rational strategy is to get an energy source that does not need subsidies to be a profitable investment. Wind and Solar cannot do this. As the numbers show, wind and solar are very large business and can survive and profit within the reduced subsidy domain. They can live happily and profitably off of current subsidies while blocking any potential competitors from any serious attention. While clean energy advocates continue to believe that wind and solar are the only answer, and consider any position that questions this as heresy, no progress can be made. By Edmund Kelly This is the Solve For <X> hosted hangout on air for StratoSolar video recording with the addition of pictures when referenced in the discussion. The length of the video and the dialogue is unaltered. |

Archives

December 2023

Categories

All

|

RSS Feed

RSS Feed

|

© 2024 StratoSolar Inc. All rights reserved.

|

Contact Us

|