|

There has been a series of recent articles that paint a picture of the improving state of the PV business. This article highlights that China is starting to deal with the zombie 2nd tier companies. The first tier like Jinko, Trina, Canadian, Sun Edison are pretty strong. This Jinko report shows them profitable with panel ASPs of $0.63/W in China. This matches well with $0.75/W in the US and Europe. China is lower cost because it has cheaper financing and cheaper labor. Also there is starting to be life in the Polysilicon market as polysilcon price has rebounded from $15/kg to $20/kg, with several new factories being announced by REC in China and GTAT in Malaysia.

China is the key. As European demand collapsed last year, China's new subsidies for local deployment provided the foundation for their PV panel makers and confidence for future stability. However if prices stay stable at current levels, more subsidy will be needed to grow the market. Projects in the US are profitable with current subsidies and apparently there is enough investor confidence in solar to support projects with IRRs below 10%. Projects in Texas have been bid at PPAs of $0.05/kWh based on low financing costs and current subsidies. Chinese panel makers are becoming project developers as a means to ensure a market for their panels, following the example of US panel manufacturers First Solar and Sunpower that have successfully used this strategy to survive with uncompetitive panels. Overall PV growth projections seem to hinge on new markets in the developing world. Panel prices should stabilize at current levels of around $0.75/W, or even rise over the next few years as the industry returns to profitability. This is all good news, but does not paint a picture where the PV market is likely to grow to the level needed to make a significant impact on CO2 emissions any time soon. By Edmund Kelly

Comments

Alternative energy exists solely because of a political will to make it so. It has been uneconomic from its modern inception in the 1970's, driven by the first oil crises. As a result, market driven economic viability has never been a central part of the alternative energy mindset. At its core it has been driven by two perceptions. The first was simply the need for a clean fossil fuel replacement largely regardless of cost. The second was that given time, costs would reduce to make them more acceptable.

The political will influenced government to provide subsidies to nurture the business. These subsidies now exceed $100B/y of investment worldwide and prop up a total investment of about $250B/y. However a business that depends so heavily on government support is subject to all the problems of such reliance. Firstly government support is volatile, driven by who wins elections. Secondly, subsidized industries are notoriously inefficient. Any long term subsidy regime encourages business that live off the subsidies with little or no incentive to improve. The perception that costs would reduce has been borne out by time, but the path has been a rocky one. The recent history of PV shows the erratic nature of this progress. On a day to day basis no one sees the big picture. When PV prices were stable for a decade, the perception was of stagnation which led to betting on thin film PV. When prices were falling the perception was they would continue to fall, regardless of fundamentals. Also, market size of a heavily subsidized industry is not perceived as inextricably tied to the size of subsidy. If government continues to support the PV business, costs will decline to a point where PV is competitive for some fraction of energy for sunny locations, but to be a complete solution other technologies like long distance transmission and storage have to become economically viable as well. The current rate of improvement put that point out beyond 2050. This is the status quo. Governments willing to provide limited subsidy, a business happy to live of this subsidy with its current size and rate of growth and an alternative energy political consensus that thinks this is actually working. This status quo is not reducing CO2 emissions and will not reduce CO2 emissions out to 2050. Realists point out that change of the degree necessary to reduce CO2 takes many decades and huge political will. While alternative energy imposes large new costs, the current small political will for change is directly measured by the small amount we are collectively willing to pay for subsidies. The only way to increase the political will is to reduce the cost at a faster rate or better yet turn things around and make clean energy an economic benefit. This perception is sadly lacking. The optimists place their hope in technological breakthroughs, and so we get daily updates on basic research, most of which we know will go nowhere, but create the illusion of progress. The sad reality is that basic research takes decades to make it from the lab to the market and decades more to achieve large scale. To scale quickly a technology needs both a long gestation to viability and to be mass producible. PV has recently demonstrated that it is at this point. The rapid scalability has surprised governments that provided subsidies assuming a slower ability to scale. Germany spent over $150B in two years for about 15GW before they adjusted. China just ramped to over 12GW in one year from a standing start for a lot less. So PV technology is at a point where we can make and deploy as much as we can afford. The problem is the high cost of the resulting electricity, especially if you count the costs of intermittency and storage, is just too much money for economies to sustain. StratoSolar is only PV in a new location. It reduces the cost of resulting PV electricity to market competitive levels and increases the reliability of the supply. There is no new technology or resource that limits its ability to scale. If it is proven viable, the major thing that needs to scale is PV manufacturing, the thing that has already demonstrated scalability. This is a lot like computers in the late 1980s. A large CMOS semiconductor manufacturing business had matured and companies like Sun Microsystems that built computers based on this technology rapidly scaled to volume in the millions. This pattern repeated itself for PCs in the 10s to 100s of millions and recently for mobile phones in the billions, as the cost of computers reduced with volume over time. The common elements are ability to scale supply and an affordable product with sufficient demand to match the supply. From an investment perspective the risk is like betting on a Sun Microsystems. They had engineering and market risk, but they were fundamentally enabled by available semiconductor technology. They were small investments in small teams that integrated existing technologies to build new products for very large new businesses. The market demand they produced could be met by the scalable semiconductor supply. Similarly, StratoSolar can create a demand that can be met by a scalable PV semiconductor supply. It’s continuing the triumph of the semiconductor age. by Edmund Kelly This is the Solve For <X> hosted hangout on air for StratoSolar video recording with the addition of pictures when referenced in the discussion. The length of the video and the dialogue is unaltered. The holy grail of alternative energy is practical, affordable energy storage. Without this, wind and solar energy can only be a partial solution to replacing fossil fuel energy. There is a growing awareness of the significance of this problem and a wide variety of technologies are gaining increased investment. However, the problem is hard and no technology as yet seems in sight of being both practical and affordable. The goal is $100/kWh, and/or $1/W with long life and high round trip efficiency. Most technologies exceed $500/kWh and have problems with life, efficiency and/or geography. The StratoSolar main page lists some companies trying new storage approaches in the 'related sites' list on the right.

StratoSolar PV electricity solved cost, reliability and geographic independence problems of Solar PV, but it still did not produce energy at night, and has been dependent on the eventual emergence of a viable energy storage technology. Over recent months we have made a very significant breakthrough in energy storage technology intimately tied to the StratoSolar solution. This new invention makes StratoSolar PV power plants complete 24/7 producers of electricity. The new StratoSolar technology is a variant of gravity energy storage. The most common electricity energy storage method is pumped hydroelectric, which is a form of gravity energy storage. This pumps a mass of water from a low reservoir to a high reservoir, storing energy as gravitational potential energy. Gravitational potential energy is mass times height times gravitational acceleration. For pumped hydroelectric storage, the height is small, measured in hundreds of meters and the mass is large. Measured in tens of thousands of tonnes. StratoSolar gravity energy storage instead makes use of the great height of platforms to store energy with relatively small masses. The height is about 20,000 meters, but the masses are measured in hundreds of tonnes. Winches raise the masses to store energy and lower them to recover energy. Each kg of mass can store about 54Wh of gravitational potential energy. Stored energy can scale with generated PV electricity. Each square meter of PV panel can generate about .9kWh/day to 1.3kWh/day, depending on latitude and gravity energy storage can easily store about 300Wh to 500Wh for each square meter. This balance of generation and storage allows a 24/7 electricity supply with the ability to respond to changing demand more quickly than expensive 'peaking generators'. This approach costs about $125/kWh today but with volume can scale to much lower cost. It also has a long life, high reliability and high round trip efficiency. So StratoSolar now provides a complete 24/7 replacement for fossil fuel electricity generation at lower cost and zero CO2 emissions. By Edmund Kelly Just a brief post that backs up previous posts on PV prices ticking up as the market stabilizes. This link is about GTM's near term PV price predictions. GTM publishes market research on the PV business. They are usually bullish and over optimistic.

This is good news for the PV business, as it means that it is finally getting to a more healthy footing after several years of disarray. This is mostly because China decided to support it's PV investments by subsidizing local demand within China. It will be interesting to see how far this goes, and also it will be interesting to see how long the recent surge in Japan lasts, now that they are adopting far more limited and realistically achievable CO2 emissions reduction goals. The deeper reality is that PV panels at these prices produce electricity that is still too expensive without subsidy in almost all markets. What is called grid parity for rooftop solar is now achievable in a few markets, but this is only because retail electricity is an overpriced monopoly in those markets. Solar with current subsidy levels is a stable business, but its not likely to grow to a size that will have an impact on CO2 emissions reduction. Hopefully the failure of over optimistic projections of PV price reductions based on short term extrapolations will sober up the eternal optimists and get some sense back into discussions of viable and realistic ways to reduce CO2 emissions. I doubt it. Published By Edmund Kelly

It's a while since I discussed the topic of subsidies. It's a difficult topic to understand, and usually provokes defensive reactions from solar energy supporters.

This recent interview with Shyam Mehta, a GTM PV researcher provides good current information and perspective on the PV business.

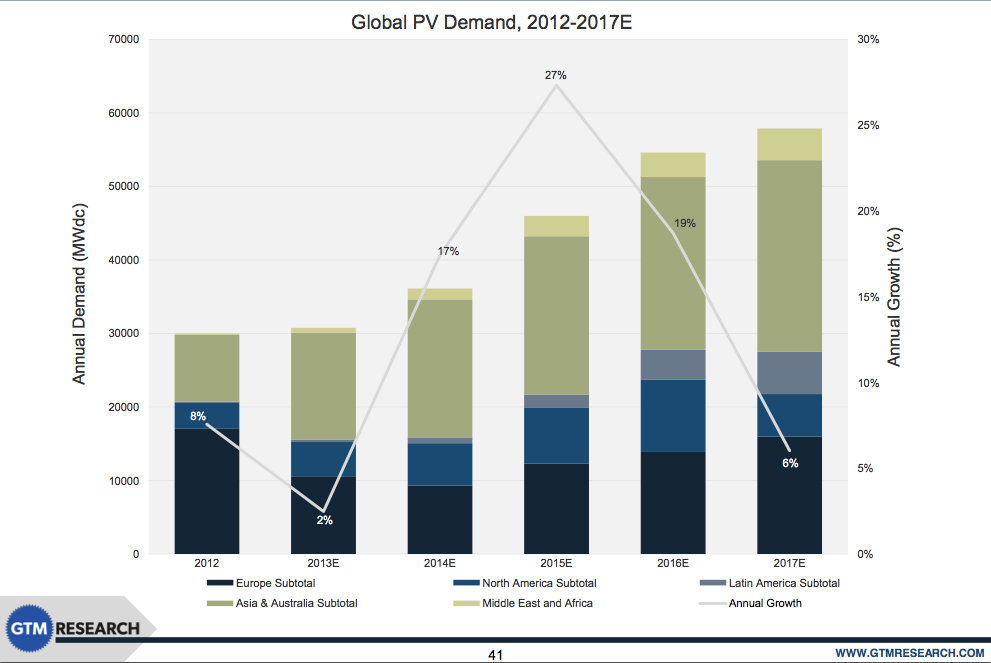

As can be seen from the chart, there were dramatic changes in the composition of PV demand from 2012 to 2013 but no overall growth in volume or revenue. Basically the PV demand went to markets where there were new or growing subsidies and left markets where subsidies declined. Overall, China probably adjusted its subsidies upward mostly to ensure their PV industry survived the drop in European demand driven by the drop in European subsidies.

This is not a well behaved or predictable market. The predictions are totally dependant on predicting subsidies. The GTM forecast is predicting that Europe will regain an appetite for increased subsidies in 2015 and beyond. Its hard to know what the basis for this is. The predicted growth in the US is based on the subsidies that are in place remaining until they diminish in 2016, when US demand is predicted to drop about 50%. The biggest unknown is Asia. Japan's commitment to expanding PV seems pretty solid at least for a few years. China's demand is hard to predict. If it mostly depends on propping up the local PV business they don't have much need to increase demand substantially going forward. Overall it seems a bit optimistic to be predicting an average 20% PV market growth over each of the next two years. Long term, subsidies would be required to grow substantially to maintain a 20% growth rate, which could see prices halve by about 2025, and the cost of subsidies leveling off. A rough estimate of the PV market in 2013 is 30GW, worth about $90B of which $50B is subsidies. If PV prices have stabilized, growth of 20%/y implies growth in subsidies to around $100B in 2017. For the US the 2013 PV numbers are about 4GW installed, worth about $12B, of which about $7B is subsidies. The projected growth implies about $14B in PV subsidies by 2016. That's about the entire alternative energy subsidies in 2013, so it will be noticed. What is the appetite for subsidies? The US spent about $150B from 2008 to 2013, or $30B/y. A lot of that was ARRA one time expenditures. 2014 subsidies are projected to total about $12B. Solar is taking more of the pie. The current US congress would not be predicted to increase alternative energy subsidies, and could easily cut them. This is all rather long winded, but the bottom line is the PV market size is completely defined by subsidies and projecting PV growth means realistically projecting increased subsidies. Given the pain level associated with today’s subsidy levels, (witness Germanys's pullback) its difficult to see significant increases in world total subsidies to the level necessary to sustain substantial PV growth. By Edmund Kelly I have written previous posts pointing out the benefits of StratoSolar for Japan and the UK, two very densely populated countries with few indigenous energy sources and a desire for clean energy.

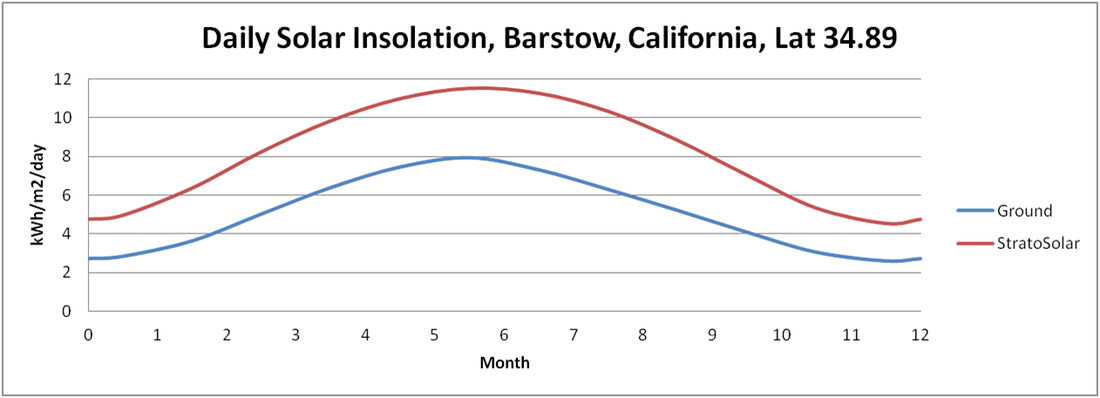

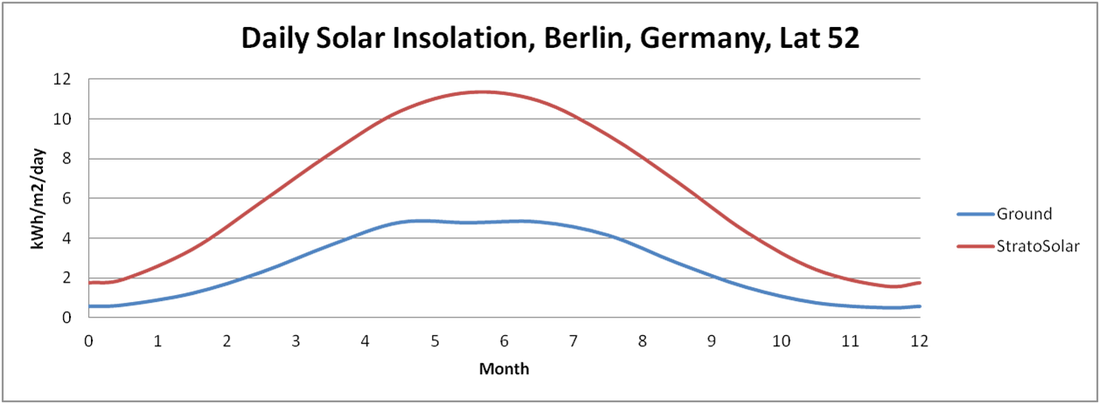

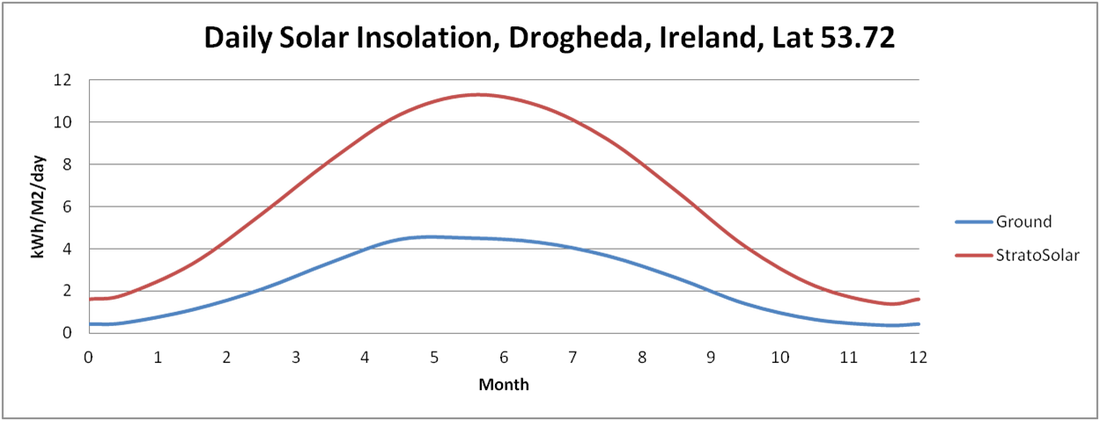

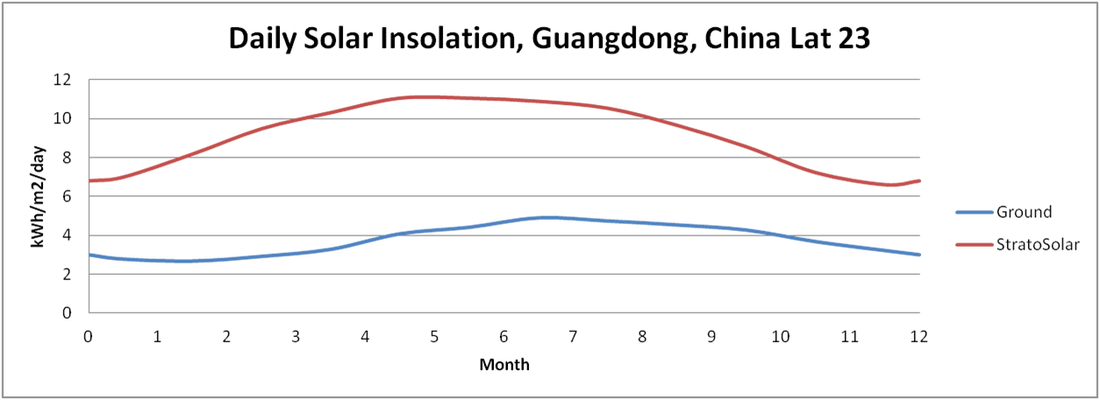

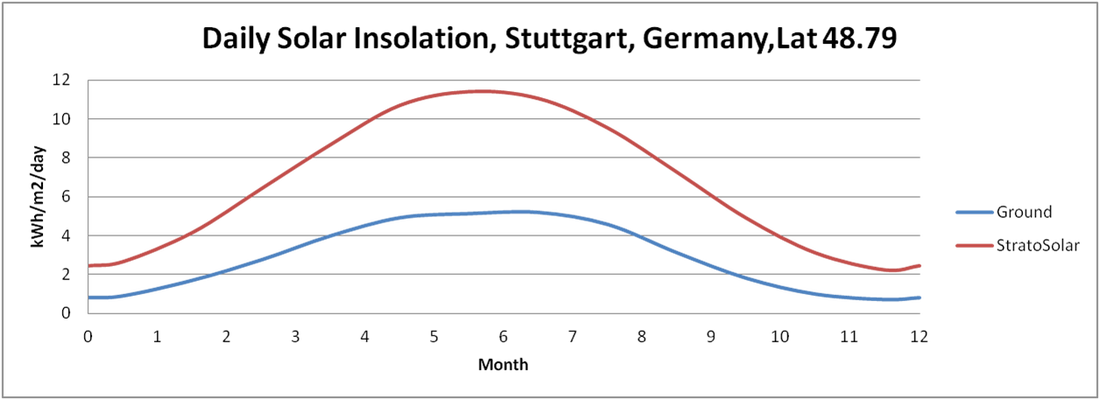

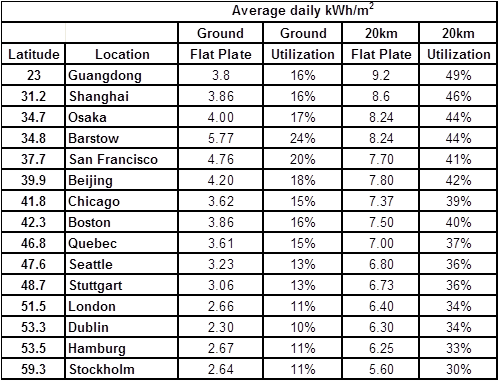

Though China is not as committed to clean energy the potential benefits of StratoSolar for China seem even more compelling, though for different reasons. In general, solar and other renewables solve three problems: 1) Fossil fuels are a finite resource. 2) Burning fossil fuels damages the environment and is causing climate change. 3) Energy security. Dependence on imported energy threatens national and economic security. Interestingly, for the US, none of these problems are currently regarded as particularly serious, and the environmental argument 2) is the only one propping up alternative energy. China is the inverse of the US. For China 1) and 3) are already a problem today, and at China's rapid rate of economic growth the problem is only getting worse. China is now the world's biggest oil importer, but its oil consumption is set to a least triple by 2040, 75% of which will be imports. This puts the Chinese economy at huge risk from oil price volatility and/or supply constraints. China has a lot of coal so coal is not in as precarious a situation, but China currently imports a lot of coal from Indonesia and Australia. An unlimited local source of cheap energy solves these problems. Not only does it remove the resource and security problem, it also potentially provides an economic competitive advantage. China has leveraged cheap coal energy into dominance of energy intensive industries like steel, aluminum and chemicals. If StratoSolar provides cheaper energy it can continue that strategy, with the added benefit of no pollution. It also puts China in a leadership position in a technology of world significance. Following the PV cost reduction path and investing in fuel synthesis technology could cement and enhance this leadership position. A quick short term benefit is StratoSolar deployment in China would help some specific industries that China has overbuilt; aluminum and PV silicon. StratoSolar systems consume a lot of aluminum for the structure, and clearly use PV panels. StratoSolar systems deployed on a large scale would rapidly become the world's biggest aluminum and PV consumer. Food for thought. By Edmund Kelly I have updated the web site main page to show graphs illustrating the extra solar energy available at 20km altitude. The visual comparison seems to be more compelling and revealing than simply quoting numbers. NASA has provided a convenient SSE database covering daily ground level solar insolation for the entire planet based on satellite data gathered over 20 years. Using this data and a model for solar insolation at 20km we show comparisons for significant urban locations at latitudes from 23 to 60 north. StratoSolar insolation is just a little less than top of atmosphere insolation which is widely available data, (including in SSE) and a convenient check on the StratoSolar estimates. A perusal of these charts shows how large and consistent the benefit of StratoSolar is. Desert level insolation is commonly used to optimistically represent solar, but the combination of a desert and a large urban area is rare, and the cost of long distance transmission offsets any benefit. California does not appreciate how lucky it is in this respect. North Africa, the Middle East and Australia are about it. An optimistic world average for ground PV utilization is 15%. The chart accompanying the graphs condenses the visual solar insolation into numbers and also provides the equivalent utilizations which are useful for estimating actual power from a given PV nameplate power. By Edmund Kelly Click for larger image

Most approaches to improving PV focus on reducing the cost and increasing the efficiency. StratoSolar instead, is based on exploiting a more solar rich environment. A comparison with two other approaches that try to exploit more solar rich environments may better help in understanding StratoSolar. The two other approaches are to exploit the sunshine in deserts and sunshine in outer space. Both have been investigated extensively and are sufficiently plausible to have received significant funding. The most notable desert project is DESERTEC, which aims to exploit sunshine in North Africa and transmit the electricity to Europe. Space based solar power (SBSP) was researched heavily by the DOE in the seventies, and revisited by NASA in the late nineties. A SBSP start-up company called Solaren obtained a PPA in 2012 from PG&E in California to deliver power in 2016.

In the DESERTEC case, the average PV utilization in North Africa is about 25% versus the average of less than 15% for the whole of Europe. The benefit is less than a factor of two overall. Offset against the benefit is the cost of High Voltage(HV) transmission over an average distance of 2000km. Given that this transmission is tied to the generation, its relatively easy to calculate the transmission cost. At today's PV costs HV transmission about matches the cost of generation. Transmission cost should reduce when HVDC transmission develops, but PV will also reduce in cost, so the ratio may not change much. DESERTEC wants to exploit Concentrated Solar Power(CSP) but CSP prices are high and not falling, so that may not work out. For Space based power, the advantage is constant almost 24/7/365 power. Measured using the ground based PV metrics, SBSP has a utilization of 130%, due to the higher intensity sunshine in space. Offset against this is the expected 50% loss in microwave conversion, transmission and receiving which could be regarded as reducing utilization to 65%. PV efficiency would be higher at a colder operating temperature. PV panel lifetimes in space are short due to damage from cosmic rays. There would be advantages to a CSP solution in space, but the complexity is significantly higher than PV. The big problem with SBSP is the very high cost of launching the material into space, and then the assembly and maintenance costs in space. StratoSolar can be viewed as an intermediate point between desert power and space power. Because of night-time interruption, its average utilization is around 40%, and can exceed 50% with one axis tracking. This is higher than the desert, but lower than space. Its transmission costs are low, 20km straight down versus 2000km from the desert or 35,786km via microwaves from GEO. Its equivalent of launch costs is gas bags full of Hydrogen which are very low cost. In the Stratosphere there is no weather or dust, very nearly like outer space, but there is still enough atmosphere to protect PV from cosmic rays, so without ground based weathering degradation or space based degradation, panels may have very long lives, exceeding thirty years. StratoSolar, unlike the desert, does not need water for washing or cooling, which adds to its major benefit over the desert in that it is situated near the demand for energy with few restrictions on where it can be situated. So when viewed against deserts and space, both of which have received considerable attention, despite significant problems, perhaps StratoSolar can be seen as a possible contender from science fact, and not something from science fiction. By Edmund Kelly |

Archives

December 2023

Categories

All

|

RSS Feed

RSS Feed

|

© 2024 StratoSolar Inc. All rights reserved.

|

Contact Us

|